T he U.S. is one of a small number of nations with the coveted rating - for now. Moody's Investors Service warned this week that the government's massive debt burden could cost the country its triple-A.

he U.S. is one of a small number of nations with the coveted rating - for now. Moody's Investors Service warned this week that the government's massive debt burden could cost the country its triple-A.

Yet the reaction from investors and the public has mostly been a shrug.

The stock market was briefly rattled, then resumed its gradual climb. And ordinary folks didn't seem to notice a report raising the possibility that their children and grandchildren face a lower standard of living thanks to mounting government debt.

A triple-A rating says a country is very unlikely to default on its debt. Like a homeowner with a good credit rating, countries with this exalted status get better interest rates when borrowing with notes and bonds.

A downgrade often means they have to offer higher rates to get investors to bite, a move that ripples through the credit markets and in turn hikes rates on mortgages, credit cards and car and business loans.

"It's a little scary," says Benn Steil, a senior fellow at the Council on Foreign Relations. The U.S. debt situation "is serious, and it needs to be addressed now."

Countries and territories in the world deemed safe enough to merit triple-A by another credit agency, Standard & Poor's, now number a mere 18 out of 123 rated. France, Germany and Britain earn top marks, as do some curiosities like the Grand Duchy of Luxembourg and the Bailiwick of Guernsey. Moody's technically calls the rating Aaa, while S&P calls it AAA.

Japan dropped out of this elite group in 2001. In March, Ireland was downgraded. Spain lost bragging rights in January.

The next step down at Moody's is Aa1. At S&P, it's called AA+. Either one would be far ahead of most other countries but still something of an embarrassment for the United States.

It's an unlikely step, money managers say. A big reason is that it's easy for the U.S. to borrow, even with high debt, because there's natural demand for Treasurys.

It's the asset of choice for central banks' reserves, a sort of rainy day fund for countries. People also like to hold dollars because it's the currency of international trade. If you want to buy oil, for instance, you need to do it in dollars.

Another reason investors are brushing off a possible downgrade: Rating agencies have warned before that the U.S. could lose its triple-A, and rates on U.S. debt have stayed low anyway.

Maybe they shouldn't be. The United States' finances aren't looking so good lately.

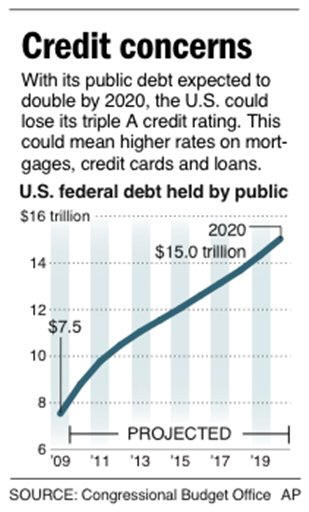

The U.S. deficit hit $1.4 trillion for fiscal year 2009, three times higher than the year before. That is 10 percent of gross domestic product, the highest since 1945. And U.S. debt held by the public, reflecting years of previous deficits, now stands at $7.5 trillion, or 53 percent of GDP

- the highest level since 1955.

Another worry: The U.S. depends on the kindness of strangers to finance the debt. Forty-eight percent of the $7.5 trillion in tradable Treasurys is held by foreigners. Japan, another big bond issuer, has just 4 percent of its debt in foreign hands.

Is it possible that overseas buyers may stop buying our debt someday? If trouble is ahead, one place to watch closely is Treasury auctions.

So far the U.S. has been able to sell its bonds at these weekly events with ease. But worrywarts point to Britain's inability to sell all the bonds it wanted to at one of its auctions last year, and the possibility of a similar "failure" for the U.S. someday.

To unload the unwanted bonds, the U.S. would have to offer higher rates.