| ||||||||||

| ||||||||||

Keith Brainard, research director for the National Association of State Retirement Administrators, says it may be unprecedented that so many states at once are raising employees' pension contribution rates.

Among the developments around the country:

Rhode Island in 2009 reduced cost-of-living increases and tightened eligibility requirements for retirement. Previously, employees could retire with 28 years of service. Now, those already employed by the state will have to meet a new standard that takes both age and years of service into account. In Wyoming, as of Sept. 1, employees will have to start paying 1.4 percent of their salaries into a pension fund

-- the first time in a decade the workers have had to contribute anything. Vermont earlier this year changed the retirement age for many current employees. They must be 65, or their age and years of service must add up to 90. Previously, retirees had to be 62 or have 30 years of service at any age. Lawmakers in Colorado, South Dakota and Minnesota rolled back cost-of-living increases this year for public employees who already have retired. In Colorado, retirees had gotten 3.5 percent annual increases. They are getting no increase at all this year, and future ones will be capped at 2 percent. Legal challenges to the cuts have been filed in all three states. "Whether legislatures have the power to change benefits for people who are already in the system, that's a tough question," said Ronald Snell, an analyst for the National Conference of State Legislatures who monitors public pension issues across the country. "It's unresolved in a lot of places."

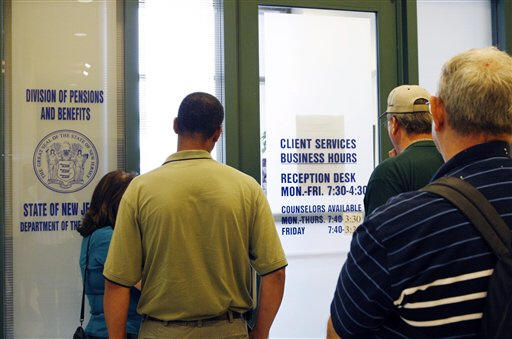

Unions are on guard against the benefit cuts -- and the implication that workers are to blame for states' financial messes. "What we don't need is more scapegoating of public service workers and their benefits," said Matt O'Connor, a spokesman for the Connecticut State Employees Association. In some states -- including South Dakota and Mississippi -- public employee retirements are up by more than 20 percent, though it is not clear whether changes to pension programs there are a factor. The retirement rush is even more dramatic in New Jersey, where by the end of July nearly 18,000 employees in the three biggest public worker pension funds had retired or declared their intent to retire this year. That is up almost 50 percent over all of last year, and several union leaders and workers considering retirement said that possible pension changes were a factor. The exodus could end up hurting the pension funds, because retired workers will be making withdrawals, not deposits into the system. Mike Ryer, a firefighter in Morris Township, was among employees in line at the New Jersey pension office around dawn one morning this summer, considering whether, at 59, he was in financial shape to retire after 32 years. He is afraid of changes in his benefits and also figures his retirement now might save a younger colleague from layoff. If he stays, he faces a smaller department and a bigger workload. He blames Christie for driving him out. "It's hard to understand why all of this had to come at once," he said.

[Associated

Press;

Copyright 2010 The Associated Press. All rights reserved. This material may not be published, broadcast, rewritten or redistributed.

News | Sports | Business | Rural Review | Teaching & Learning | Home and Family | Tourism | Obituaries

Community |

Perspectives

|

Law & Courts |

Leisure Time

|

Spiritual Life |

Health & Fitness |

Teen Scene

Calendar

|

Letters to the Editor