| |||||||||||

| |||||||||||

Sometimes they forged the signatures of executives who were qualified to sign. Other times, actual executives signed the documents without verifying their accuracy. Many of the documents were stamped by notaries even though the people who had signed the documents weren't present when the papers were notarized, a requirement by law. All are instances of robo-signing, and are potentially illegal. The 50 state attorneys general have been negotiating a settlement with major lenders over robo-signing and other bad mortgage practices. Analysts say it could top $20 billion. But the attorneys general of some states, including New York, Massachusetts, Illinois, Delaware and California, have balked because banks have demanded a release from all future liability on past mortgage practices or the mortgage-backed securities they sold to investors. Meanwhile, federal bank regulators have focused on getting banks to clean up their act in the future, not on fixing the potentially millions of tainted documents that have been filed in land record offices in counties across the country. Robo-signing came to light last fall, when the largest banks halted foreclosures for several months to clean up their paperwork problem. The lenders promised last fall to stop the practice. But The Associated Press reported in July that robo-signing has continued. Officials in at least four states say mortgage documents with suspect signatures have been filed with counties in recent months. The revelation led to calls for Congressional hearings.

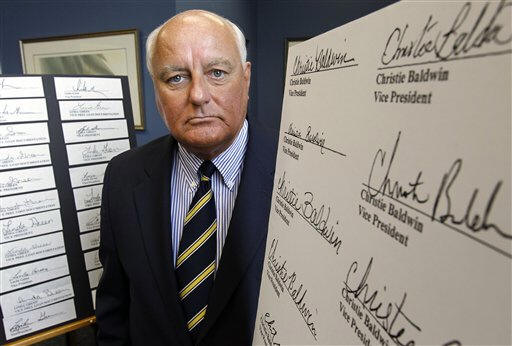

On Thursday, the mortgage unit of Goldman Sachs Group Inc. agreed to stop robo-signing and other controversial mortgage practices under an agreement with New York state's banking regulator. The Federal Reserve, meanwhile, launched a formal enforcement action against the unit, Litton Loan Servicing, ordering it to review foreclosure proceedings from 2009 and 2010. "The banks are playing with the integrity of the land record system," says John O'Brien, the recorder of deeds from Salem, Mass. The documents that are filed in county deed offices are legal affidavits that transfer loans from one bank to another in a sale, refinancing, or foreclosure and certify if a loan has been paid off. They verify that there are no claims against the property. Robo-signing could ultimately invalidate tens of thousands of home ownership documents, say legal experts. In addition to delaying regular sales, banks could be blocked from foreclosing even if the homeowner falls behind on mortgage payments for the same reasons. That's already happening. Judges who handle foreclosures in Maine, California, Arizona, New York and other states have thrown out foreclosure cases if documents contain signatures of known robo-signers. On July 1, a state judge in Brooklyn ruled that HSBC lacked the legal authority to foreclose on homeowner Ellen Taher because the mortgage documents that accompanied the filing were signed by at least three known robo-signers. In May, a Maine judge dismissed another foreclosure involving HSBC, calling mortgage documents presented in a case untrustworthy because they contained signatures of one person posing as three different people. HSBC spokesman Neil Brazil says another company handled the mortgage paperwork in the New York case, and the bank is working with regulators to address and resolve issues related to robo-signing. Registrars like Thigpen in North Carolina and O'Brien in Massachusetts say they have taken their findings to federal authorities. Except for a call from the North Carolina attorney general's office, though, Thigpen says he has been ignored for months.

Deed offices in North Carolina and Massachusetts have stopped recording documents if they contain signatures of names known to be part of the robo-signing scandal. Such actions could delay new sales. O'Brien, the recorder of deeds from Massachusetts, says he's only responsible for one county out of more than 3,000 in the U.S. "Federal regulators with a lot more authority than me have to step up to the plate and help correct this," he says.

[Associated

Press;

Copyright 2011 The Associated Press. All rights reserved. This

material may not be published, broadcast, rewritten or

redistributed.

News | Sports | Business | Rural Review | Teaching & Learning | Home and Family | Tourism | Obituaries

Community |

Perspectives

|

Law & Courts |

Leisure Time

|

Spiritual Life |

Health & Fitness |

Teen Scene

Calendar

|

Letters to the Editor

The suspect documents could create legal trouble for homeowners for years.

The suspect documents could create legal trouble for homeowners for years.