The past six audits were performed by

Clifton Gunderson (now Clifton Larson Allen), with Helen Barrick as

the lead auditor. Barrick began working with the county as a

consultant to help bring in a difficult audit being performed by

another firm for the year 2005. As Barrick is preparing to retire

next year, she brought in Jeff Bonack and Adam Pulley to work this

past year and they will also work with her next year. The past six audits were performed by

Clifton Gunderson (now Clifton Larson Allen), with Helen Barrick as

the lead auditor. Barrick began working with the county as a

consultant to help bring in a difficult audit being performed by

another firm for the year 2005. As Barrick is preparing to retire

next year, she brought in Jeff Bonack and Adam Pulley to work this

past year and they will also work with her next year.

As a bonus tool that might aid county administrators, Bonack and

Pulley compiled figures from the past five audits and put them into

comparative graphs. They also added brief summary statements for

significant differences between 2010 and 2011 figures, "just to give

you an idea of where you are at today, versus a couple of years

ago," Bonack said.

Figures in the special report include property taxes; income

taxes; sales taxes; motor fuel taxes; user charges, fees and fines;

operating and capital grants; and total expenditures, cash and

cash equivalence; certificates of deposit, at cost; receivables;

capital assets; notes, leases, bonds and compensated absences

payable; other liabilities; deferred revenues; and total net assets.

Included below are links to graphs that demonstrate revenue and

expense trends. These figures illustrate how the economy took a dive

late in 2007, as well as actions that were taken to increase

revenues that would help keep departments operating and services

intact.

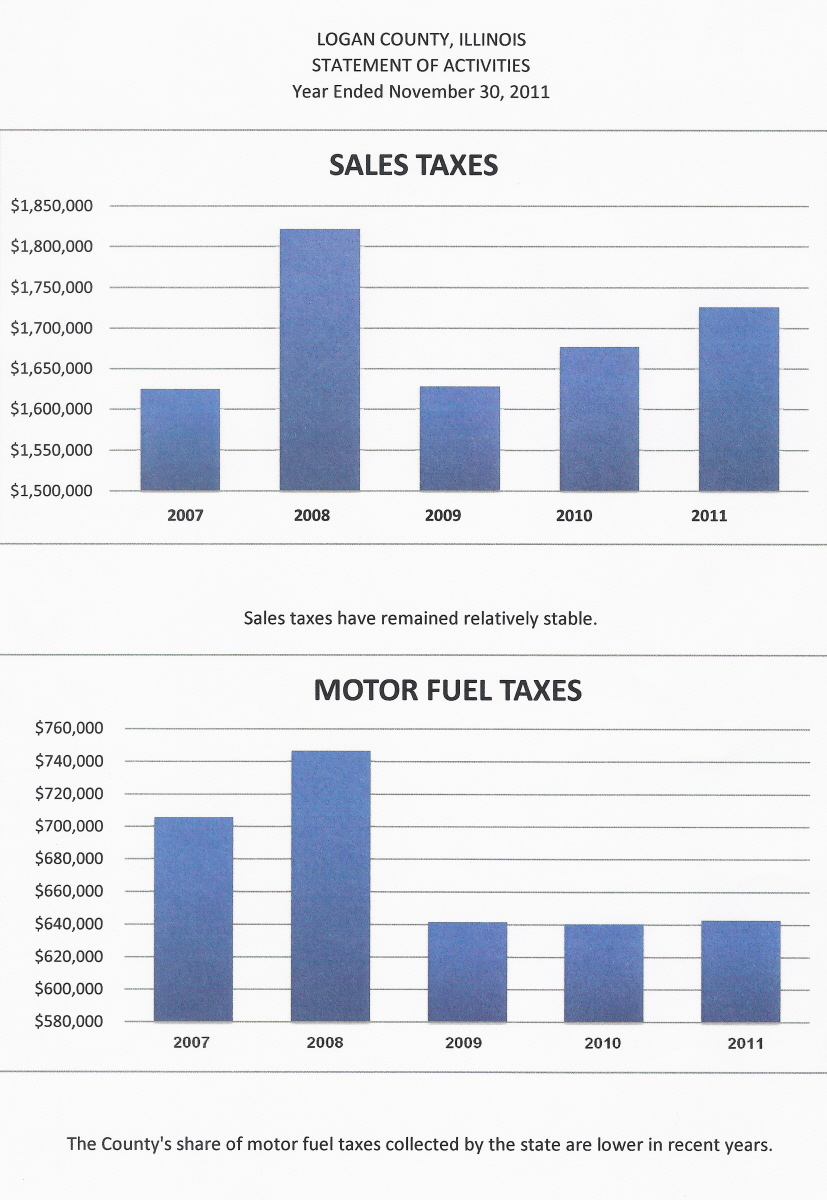

For example: The graph of sales tax shows a big drop in revenue

in the year 2008. And then you can see the slow recovery that has

been in process in the years that follow.

Revenues and expenses:

Property, income, sales and motor fuel taxes; user charges, fees

and fines; operating and capital grants; and total expenditures

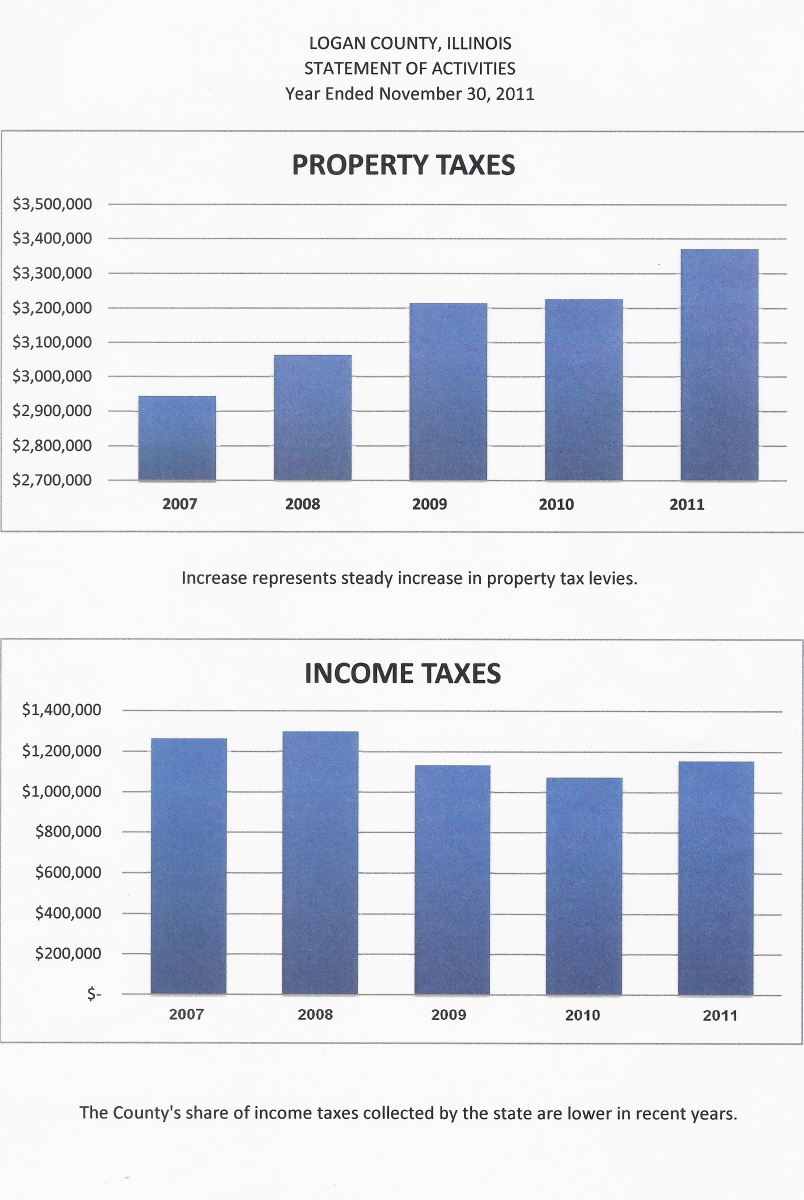

See graphs of property and income taxes.

Property taxes increased about $400,000. Income taxes were down

about $100,000 over a four-year period.

Income taxes in 2007 were $1,250,000, peaked just a little higher

in 2008, then declined, and this audit year (2011) shows the start

of recovery.

See graphs of sales and motor fuel taxes.

Motor fuel taxes:

Motor fuel taxes can only be used in a specific manner and are a

primary resource for road and bridge projects. While costs of

oil-based products used for road maintenance and renovations

continue to skyrocket, revenues from motor fuel taxes have dropped

considerably.

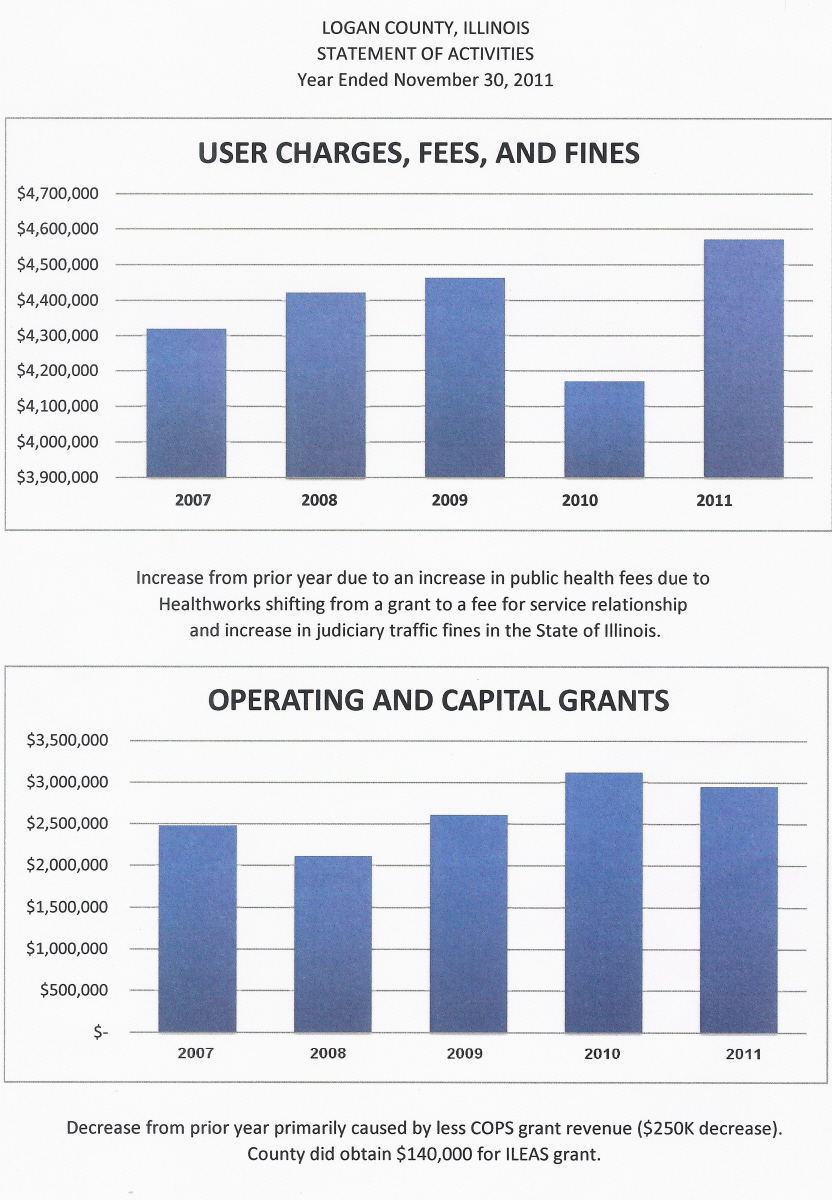

See graphs of user charges, fees , and fines; and operating and

capital grants.

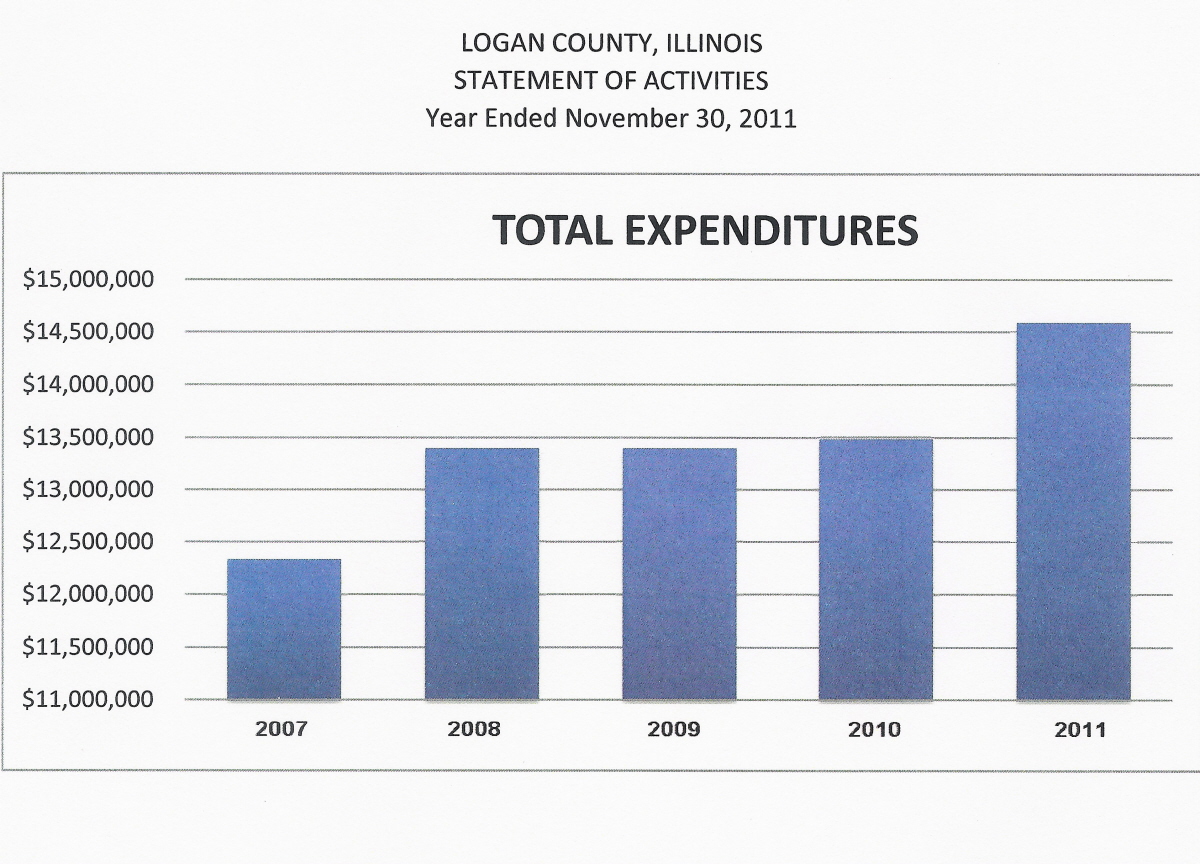

See graph of total expenditures.

Total expenditures continue to increase from $12.4 million

in 2007, reaching $14.6 million in 2011.

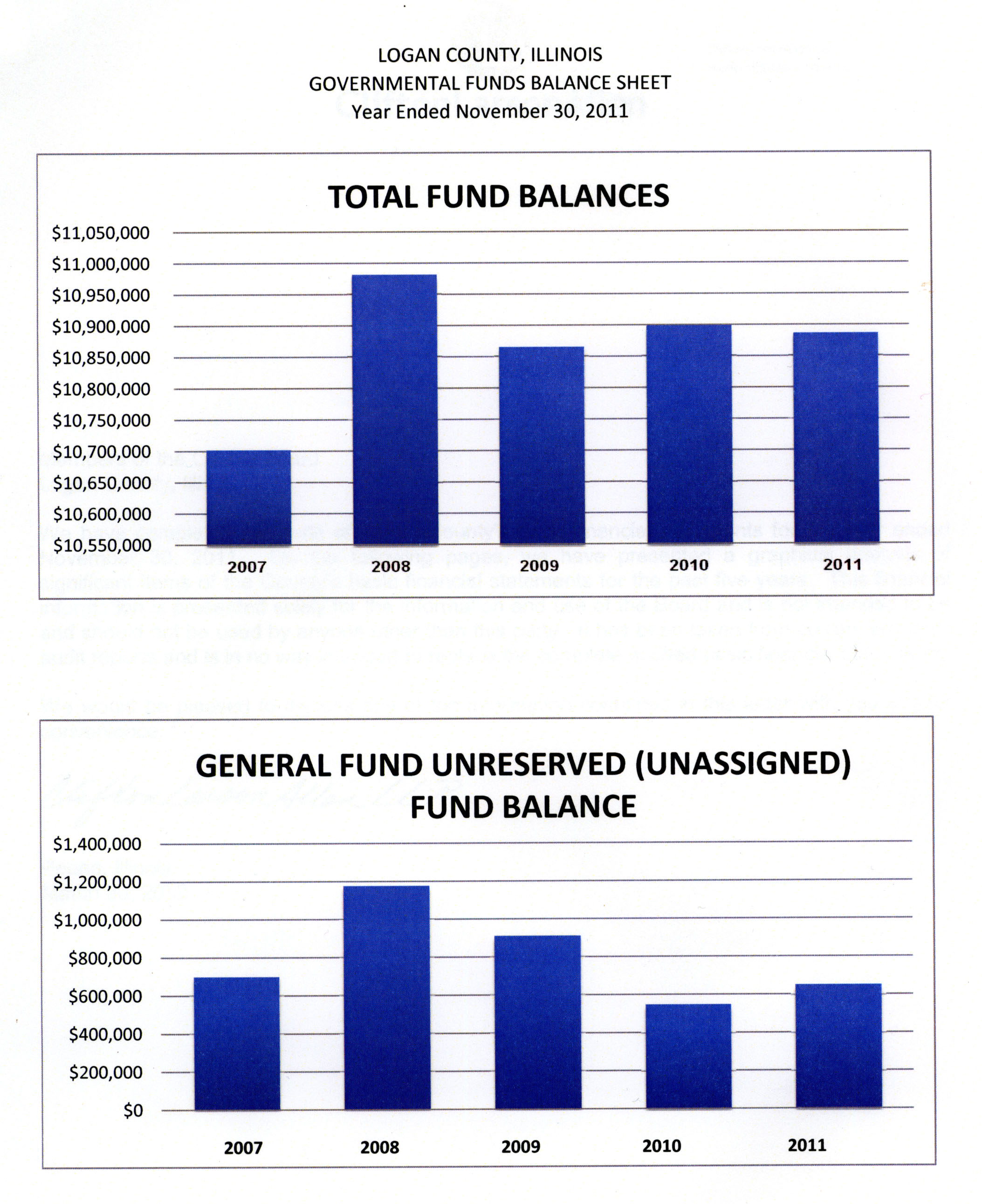

See graphs of total fund

balances and general fund unreserved (unassigned) fund balance.

The general fund unreserved reflects just over one month's

expenditures. As a guideline, the equivalent of three months '

expenditures is good to shoot for, Bonack said.

Other graphs that were included in the report but are not shown

here would benefit the county's financial planners as they prepare

their next budget.

Below is a brief summary of that information:

Cash and cash equivalence for the total of county operations

-

2007 -- Roughly $3.2 million.

-

2011 -- Came up to $4.5 million, for an increase of about $1.3

million over a four-year period. Some of those funds came from CDs,

which in '07 totaled $6.4 million.

[to top of second column] |

Certificates of deposit, at cost

The CDs went to cash, going down about $700,000 to about $5.8

million in the past four years.

Receivables

Salary reimbursements from the state, grants from the state, and

sales, income and property taxes were delayed.

Capital assets

The county reports started capitalizing infrastructure in 2004.

Infrastructure today represents $3.8 million, or about half of the

county 's capital assets.

Notes, leases, bonds and compensated absences payable

The 2007 figure was at $1,250,000, which has decreased about

$400,000 over the last four years to roughly $850,000.

Other liabilities were about $400,000 in 2007 and are right

around $1 million now. Some of that was related to a net pension

obligation a couple of years ago, as well as a timing issue on

accounts payable, which was up a bit the last year.

Deferred revenue

-

2007 -- $3.1 million

-

2010 -- $3.5 million

There was an increase in tax levies, mostly from property taxes.

Total net assets

The figure for overall assets or equity was $15.4 million in

2007. It is now $17.5 million in capital assets, an increase of $2.1

million.

There are three major categories:

-

$7.4 million in equity in capital assets

-

$3.2 million in unrestricted

-

$6.9 million in restricted

In a quick review, Barrick commented that each year would vary as

to how much money would be desired to have in hand in conjunction

with road plans, structures or capital projects. As a reminder, she

said that the end of the year is when the most revenue comes in for

most counties, and it can become lean before property taxes would

come in.

"You are moving in the right direction here," Barrick said.

[By

JAN YOUNGQUIST]

Past related articles

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}