New auto safety technology leaves insurers in the dark

Send a link to a friend

Send a link to a friend

[July 26, 2019] By

Tina Bellon [July 26, 2019] By

Tina Bellon

RUCKERSVILLE, Va. (Reuters) - Automakers

are accelerating the rollout of technology designed to avoid crashes,

but insurance companies are waving a caution flag at consumers eyeing

discounts for buying collision-avoiding brakes or automated cruise

control.

The global market for advanced driver assistance systems, known in the

industry as ADAS, is expected to reach more than $67 billion by 2025,

growing more than 10 percent each year. A group of 20 carmakers has

pledged to outfit almost every new vehicle with forward collision

warning and city-speed automatic emergency braking by 2020.

Government mandates to install technology such as collision avoiding

automatic brake systems are driving the market, as is the promise of

profits for these higher-margin vehicles.

"Anybody that has been in a car with advanced safety solutions is not

going to go back," Kevin Clark, chief executive of auto technology

supplier Aptiv PLC told Reuters. The cost for advanced safety systems -

automatic braking, lane keeping and automated cruise control - can be

relatively low to the automaker, between $500 to $1,000 per vehicle,

Clark said.

"The (manufacturer) can price for it and consumers will pay for it," he

said.

For a graphic, click https://tmsnrt.rs/2MfpRE6

Aptiv expects to book more than $4 billion in new ADAS business this

year. "We have gone from five customers just a few years ago to I think

we’ll have north of 20 in a couple of years from now," Clark said.

The insurance industry's perspective is different.

Personal auto insurance, while traditionally a low-margin business,

provides the largest amount of liquidity to insurers, generating more

than $244 billion in 2018 direct premiums in the United States alone,

data by the National Association of Insurance Commissioners showed.

Motor insurance is also seen as a way for insurance companies to

cross-sell other, more lucrative products to customers.

According to Swiss Re AG, the world's largest auto reinsurer, and

mapping company HERE, ADAS has the potential to reduce motor accident

frequencies by up to 25%, cutting global insurance premiums for fully

ADAS-equipped cars by $20 billion by 2020.

But U.S. insurers said they currently do not have sufficient data to

validate auto industry promises of safety benefits from automated

driving systems.

They cite car manufacturers' reluctance to provide detailed information

on models sold with those features, a lack of consistent standards,

drivers' unpredictable use of the systems and higher repair costs.

"We're not going to go against the data and create any type of false

discounts for the purposes of marketing at this point. We just want to

make sure the rate is reflective of the risk that it brings," said Steve

Armstrong, a vice president of Allstate Corp's pricing department, one

of America's largest insurers.

Shantelle Thomas, also a vice president at Allstate's pricing

department, said insurance rates will reflect benefits and costs of

modern auto technology in the next five years, but will not necessarily

be presented as discounts.

The sentiment was echoed by other insurance providers.

"We're stuck in a murky in-between," said Jennifer St. John, national

auto claims leader at Westfield Insurance. "ADAS have shown to provide

real world benefits, but there really isn't a great deal of commonality

in terms of what's out there."

Insurers pointed to higher repair costs as a risk. Sensors and cameras

central to automatic driving systems are mostly installed in a car's

bumper or windshield. Research by AAA has shown repair costs for even

minor collisions can double if such sensors are damaged.

"There's no such thing as a $300 bumper anymore. It's closer to $1,500

in repair costs nowadays," said Richard Lavey, executive vice president

at The Hanover Insurance Group.

[to top of second column] |

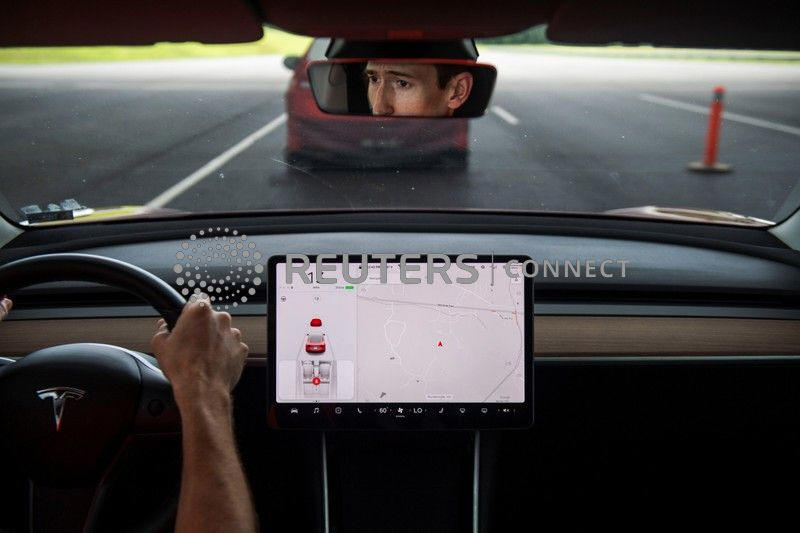

Joe Young, media relations associate for the Insurance Institute for

Highway Safety (IIHS), demonstrates a front crash prevention test on

a 2018 Tesla Model 3 at the IIHS-HLDI Vehicle Research Center in

Ruckersville, Virginia, U.S., July 22, 2019. Picture taken July 22,

2019. REUTERS/Amanda Voisard

State Farm in a statement said it did not offer discounts specific to advanced

driver assistance systems and that future rates would be shaped by a variety of

factors, including safety, regulation, underwriting, liability and repair costs.

GEICO did not respond to requests for comment.

DATA DESERT

With new automated driving features being released on a rolling basis, insurers

said it is difficult to keep up.

Forward collision warning with automatic braking has been found to have one of

the greatest safety benefits among various driver assistance systems. The

Insurance Institute for Highway Safety concluded in a recent study that

automatic braking could reduce front-to-rear crashes with injuries by 56%.

But most ADAS features are still sold as optional equipment, making it

impossible for insurance companies to validate which features ultimately end up

on a specific car. Insurers are reluctant to trust car buyers to correctly

identify what technology their vehicle has on board.

Advanced safety features not only differ in performance and description among

different manufacturers, but even among models by the same automaker, according

to research by IIHS and its UK equivalent Thatcham Research, which conduct road

tests to evaluate safety tech performance.

"The only way you can adequately price is by getting more data to understand

what a vehicle has and whether it makes a difference," said Matthew Avery,

Thatcham's research director.

That data is not sufficiently provided by manufactures who often cite

proprietary and competitive reasons, said Tom Karol, general counsel of the

National Association of Mutual Insurance Companies, whose members insure more

than 170 million U.S. auto policyholders.

Automakers and insurers said they are dealing with the data issues. General

Motors Co has a team working on ADAS and insurance, according to Barry Engle,

head of GM's North American operations.

Engle said he expects with better information, the insurance industry would

respond positively. "To the extent that they are not, collectively we need to do

a better job of communicating with one another," he said.

Swiss Re is leading efforts to develop a global ADAS risk score and a mechanism

allowing carmakers to supply data to Swiss Re, which in turn will recommend

discounts to auto insurers.

"If we say these cars are safer, insurers are more prone to believe us as we

take part of the risk" as a reinsurer for consumer-facing auto policy writers,

said Sebastiaan Bongers, Swiss Re's head of products and technology.

Bongers believes reductions in accident frequency and severity will eventually

offset higher repair costs. But he said lower premiums could result in temporary

liquidity problems in the insurance sector in about ten years.

Swiss Re so far has partnered with Germany's BMW and is in talks with more auto

manufacturers to develop a comprehensive system.

(Reporting by Tina Bellon; Additional reporting and editing by Joe White;

Editing by Edward Tobin)

[© 2019 Thomson Reuters. All rights

reserved.] Copyright 2019 Reuters. All rights reserved. This material may not be published,

broadcast, rewritten or redistributed.

Thompson Reuters is solely responsible for this content. |