Standard U.S. economic weapons may be inadequate for

coronavirus crisis

Send a link to a friend

Send a link to a friend

[March 07, 2020] By

Howard Schneider, Jonnelle Marte and Lindsay Dunsmuir [March 07, 2020] By

Howard Schneider, Jonnelle Marte and Lindsay Dunsmuir

NEW YORK/WASHINGTON (Reuters) - As the

risks of the coronavirus outbreak continue to rise, U.S. officials are

wrestling with what to do in the worst-case economic scenarios, if large

numbers of people can't go to work, are told to stay home, or stop going

out in public entirely.

In Washington on Friday, Trump administration officials pledged to step

in with "timely and targeted" help for workers and small businesses if

incomes take a hit.

Federal Reserve officials, meanwhile, broached ideas beyond interest

rate cuts, such as urging banks to relax rules governing debt payments

or pushing Congress to let the U.S. central bank buy assets other than

government securities if specific markets come under stress.

Both the Fed's short-term interest rate and long-term bond yields are

near zero, leaving little room for the central bank to help the economy

by lower borrowing costs for households and businesses, Boston Fed

President Eric Rosengren said.

"I think we need to think broadly about what tools we would use," if the

impact of the virus persists, Rosengren said during an economics

conference in New York at which Fed officials were peppered with

questions about their preparations, and asked to address worst-case

health scenarios in which tens of millions would be dead.

Rosengren, noting the work of other academics, said it "could be

important" to let the Fed buy assets other than U.S. Treasury and

mortgage-backed securities, as a way to buttress stressed markets.

That would require a controversial change in federal law, and to broach

it even hypothetically points to the fogbound horizon facing economic

policymakers.

At this point key health statistics about the coronavirus, such as its

transmission rate between individuals, remain uncertain. Consequently,

so does any estimation of the economic fallout, which will hinge on how

broadly it spreads and how long it circulates.

The number of people around the world infected with COVID-19, the virus

that causes the flu-like illness, has surpassed 100,000. More than 3,400

people have died in the outbreak.

EXPECTING THE WORST

A blockbuster U.S. jobs report for February showed part of the dilemma

for policymakers. Major macroeconomic data are backward-looking and have

yet to show a hit from the outbreak. Only a few hundred cases and 15

deaths have been reported in the country so far.

Economists scouring real-time data have had trouble finding any clear

problems so far, either.

A drop in recent movie box office receipts, JP Morgan economists noted,

may show people avoiding theaters. Or it may simply be the product of

"the popularity of recently-released movies ... It is not yet clear if

there is much decline beyond normal noise in the data."

Financial markets globally are expecting the worst and economic

forecasters have raised their expectations of a U.S. recession this

year. Stock indexes continued to plummet and long-dated U.S. Treasury

bond yields fell to fresh record lows on Friday.

Standard emergency actions such as a lowering of interest rates or

on-the-fly tax cuts are meant to lower the cost of credit, enabling

businesses and households to borrow and invest, or put money into

people's pockets for them to spend.

[to top of second column] |

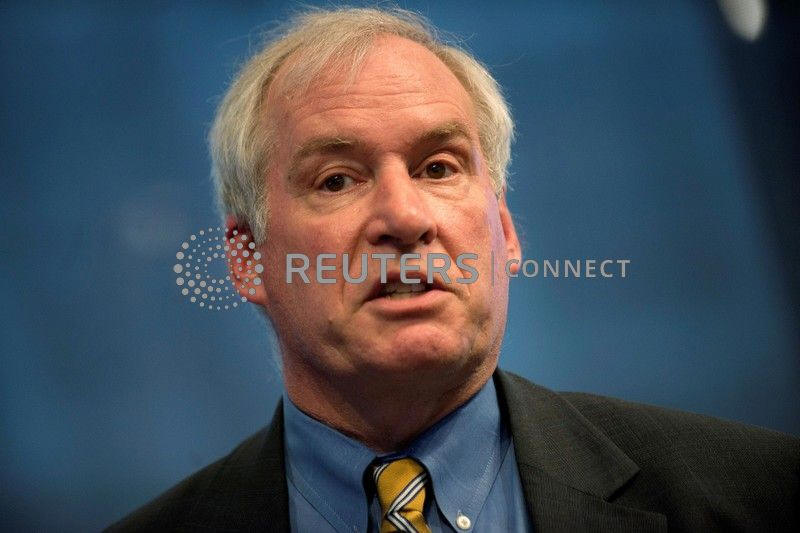

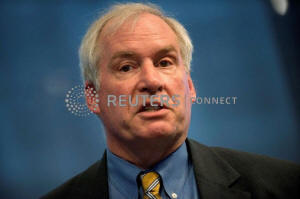

The Federal Reserve Bank of Boston's President and CEO Eric S.

Rosengren speaks in New York, April 17, 2013. REUTERS/Keith

Bedford/File Photo

But a different discussion occurs if economic activity has ground to a full

stop: how to keep small businesses from failing, how to keep homeowners or

businesses who lose income from defaulting on debts, and how to keep workers

without paid sick time from ending up bankrupt, or hungry and homeless.

"There are a lot of scenarios that could play out," depending on the spread of

the disease, its intensity, and the public health response, Cleveland Fed

President Loretta Mester said at the Shadow Open Market Committee economics

conference in New York on Friday.

Chicago Fed President Charles Evans said the response may need to go beyond rate

cuts to focus on how to get cash in the hands of people "who need it most."

That is a move that would come from the U.S. Congress and Trump administration,

not the Fed.

The policy options are "not that unclear. We just don't know what the state is,

what we are responding to," Evans said. "The most effective tools would be

getting some type of liquidity in the hands of people who need it most."

The Fed could work with banks to encourage loan forbearance for households or

companies who can't make payments. Corporate debt has risen about 80% in the

last decade, to $6.5 trillion. Dallas Fed President Robert Kaplan has noted that

if companies have trouble making debt payments, it could turn a modest slide in

the economy into a deeper downturn if it starts to hurt the financial health of

lenders.

Treasury Department officials say they are considering possible help to small

businesses or assistance to those workers without sick leave or at risk of

losing income, filling gaps likely to be laid bare if the coronavirus crisis

escalates.

Any program would be "timely and targeted for where it would do the most good,"

rather than involve a massive federal fiscal response, Larry Kudlow, the White

House's top economic adviser, said on Friday.

What is becoming clear is that a crisis that drives people indoors, and away

from jobs, stores and public events, won't be offset by "conventional monetary

and fiscal options," Oxford Economics economist Adam Slater wrote.

Fed policymakers and other officials may instead need to venture deep into

credit markets to ensure, for example, that a temporary loss of income doesn't

bankrupt households or that a small business can weather a temporary shutdown.

For the U.S. central bank, which is often the front line in fighting economic

crises, the fact that its policy rate is already so low while long-term bond

yields are diving towards zero, means there is "practically no room at all ...

to respond to a much larger contraction," than may already be underway,

Dartmouth College professor Andrew Levin wrote in a paper prepared for the

conference at which the Fed officials spoke.

(Reporting by Howard Schneider and Jonnelle Marte in New York and Lindsay

Dunsmuir in Washington; Editing by Heather Timmons and Paul Simao)

[© 2020 Thomson Reuters. All rights

reserved.] Copyright 2020 Reuters. All rights reserved. This material may not be published,

broadcast, rewritten or redistributed.

Thompson Reuters is solely responsible for this content. |