Analysis: U.S. banks' bond bonanza driven by extraordinary market

conditions, regulatory decisions

Send a link to a friend

Send a link to a friend

[April 21, 2021] By

Pete Schroeder [April 21, 2021] By

Pete Schroeder

WASHINGTON (Reuters) - Record-breaking Wall

Street bank bond offerings in recent days are being driven by a

combination of extraordinary market conditions and regulatory decisions

that can be traced to the government's pandemic relief efforts, said

analysts.

JPMorgan Chase, Bank of America, Goldman Sachs and Morgan Stanley have

or are planning to issue a total of $40 billion in debt, according to

media reports. JPMorgan's $13 billion April 15 bond sale was briefly an

industry record until it was topped the next day by Bank of America's

$15 billion offering.

While the banks did not provide details on why they are raising the

debt, analysts said a confluence of monetary and regulatory factors are

driving the unprecedented cash grab, underscoring the increasingly

tricky balancing act for Wall Street lenders as the economy emerges from

the pandemic slump.

That economic rebound driven by the vaccination roll-out and trillions

of dollars of stimulus, combined with ultra-low interest rates, has made

for excellent borrowing conditions on the heels of stellar first-quarter

earnings.

After the U.S. Federal Reserve said in March that it would lift capital

distribution curbs on banks that pass its June stress tests, many also

want to have enough cash on hand to keep shareholders happy with

increased stock buy backs.

"We are going to buy back a substantial amount ... as soon as we can,"

Bank of America Chief Executive Brian Moynihan told analysts during the

bank's earnings call prior to the bond sale.

GROWING DEPOSITS

But it's not all good news. While the fire-hose of government stimulus

gushing through the economy flattered bank earnings, it has also reduced

loan growth and caused deposits to surge. In turn, banks have had to

park those deposits with the Federal Reserve and in safe-haven assets

such as U.S. Treasuries.

"These deposits are growing like crazy, but loans are not and common

equity is not, and that creates a serious problem for the banks," said

Dick Bove, an analyst with Odeon Capital Group.

"I've never seen this happen before."

[to top of second column] |

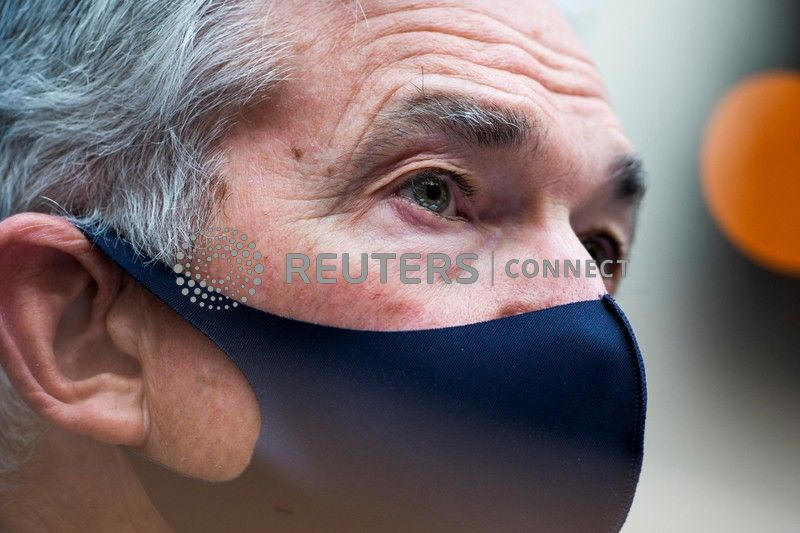

Federal Reserve Chair Jerome Powell testifies before a House

Financial Services Committee hearing on "Oversight of the Treasury

Department's and Federal Reserve's Pandemic Response" in the Rayburn

House Office Building in Washington, U.S., December 2, 2020. Jim Lo

Scalzo/Pool via REUTERS

For some banks, those problems are regulatory. As of April 1, banks had to

resume holding extra capital against Treasuries and Fed deposits after the

central bank ended temporary pandemic relief that had allowed lenders to exclude

those assets from a key capital calculation.

That "supplementary leverage ratio" (SLR) is an extra safeguard introduced

following the decade-ago financial crisis that requires big banks to hold cash

against assets regardless of their risk. With surging deposits, some banks may

be looking to raise debt to ensure they operate comfortably within the ratio.

"It's quite likely that the debt issuance may have been partly driven by the

expiration of the SLR relief," said Gennadiy Goldberg, senior rates strategist

with TD Securities.

Bank of America executives said on its first quarter earnings call prior to the

bond sale that it still had room before it hit its leverage ratio threshold. The

bond sale was primarily aimed at the bank's business growth, including share

repurchases and resolution planning, according to a person familiar with the

matter.

Morgan Stanley's debt offering was not driven by regulatory constraints,

according to a person familiar with the matter. A spokesman for Goldman Sachs

did not respond to a request for comment. The Fed declined to comment.

JPMorgan, for its part, issued the bonds in part to address regulatory

constraints, according to one person familiar with the matter. On its earnings

call, the bank's executives flagged that deposit growth had increased its

leverage, prompting Chief Financial Officer Jennifer Piepszak to criticize the

rules.

"Raising capital against deposits and/or turning away deposits are unnatural

actions for banks, and cannot be good for the system in the long run."

(Reporting by Pete Schroeder; additional reporting by Megan Davies; editing by

Michelle Price and Nick Zieminski)

[© 2021 Thomson Reuters. All rights

reserved.] Copyright 2021 Reuters. All rights reserved. This material may not be published,

broadcast, rewritten or redistributed.

Thompson Reuters is solely responsible for this content. |