|

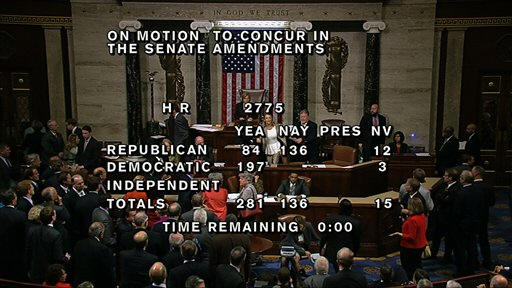

The deal approved late Wednesday by Congress, with hours to go before the government reached its $16.7 trillion debt limit, only permits the Treasury to borrow through Feb. 7 and fund government through Jan. 15. The International Monetary Fund appealed to Washington for more stable long-term management of the nation's finances. The deal approved late Wednesday by Congress, with hours to go before the government reached its $16.7 trillion debt limit, only permits the Treasury to borrow through Feb. 7 and fund government through Jan. 15. The International Monetary Fund appealed to Washington for more stable long-term management of the nation's finances.

The standoff rattled global markets and threatened the image of U.S. Treasury debt as a risk-free place for governments and investors to store trillions of dollars in reserve. Few expected a default but some investors sold Treasurys over concern about possible payment delays and put off buying stocks that might be exposed to an American economic downturn.

IMF managing director Christine Lagarde welcomed the deal but said the shaky American economy needs more stable long-term finances.

"It will be essential to reduce uncertainty surrounding the conduct of fiscal policy by raising the debt limit in a more durable manner," Lagarde said in a statement.

The Tokyo stock market, Asia's heavyweight, gained 0.8 percent Thursday. Markets in South Korea, Australia and Southeast Asia also rose.

Such relief might be only temporary without a long-term settlement, said Standard Chartered economist Samiran Chakraborty in Mumbai.

"In three months' time, this could be back again," said Chakraborty. "If this kind of pushing it back happens several times, then this comfort that the markets had over the last 20 days that a deal will be reached, that comfort may now be dead."

Also, the congressional cliffhanger might dent longer-term confidence in American government debt, a cornerstone of global credit markets, prompting creditors to demand higher interest.

"With the U.S. government's antics, the risks go up, so the cost of money could go up too," said Nick Chen, managing partner of Taipei law firm Pamir Law Group.

Big Asian exporters including China and South Korea also faced the risk of a slump in global demand if a U.S. default had disrupted other economies.

China's government, Washington's biggest foreign creditor with $1.3 trillion invested in Treasurys, welcomed the end to the standoff.

"This issue concerns many countries in the world," said a foreign ministry spokeswoman, Hua Chunyin, speaking at a regular briefing. "The United States is the biggest economy in the world. For them to handle the issue properly is to their own interest and beneficial to their own development. We welcome their decision."

China's official Xinhua News Agency issued a scathing commentary accusing American leaders of failing to address chronic budget deficits. It said their deal only makes "the fuse of the U.S. debt bomb one inch longer."

"Politicians in Washington have done nothing substantial but postponing once again the final bankruptcy of global confidence in the U.S. financial system and the intactness of dollar investment," the commentary said.

[to top of second column] |

Chen Ju, an employee at a Shanghai fast-food company, said she sold stocks when she heard the U.S. government shut down. She said she was ready to get back into the market but would look for safety.

"I just think the U.S. is crafty. They released all kinds of information. It made me confused about what was true or not," said Chen.

In South Korea's capital Seoul, 26-year-old college senior Lee Boo-gun said he thought the U.S. economy was going belly up and was relieved to hear that a deal was reached.

"I thought it would affect Korea's economy. The U.S. would hit Europe and then it would affect Asia," he said.

Martin Hennecke, chief economist at The Henley Group, a financial advisory firm in Hong Kong, expressed exasperation at what he said was a failure by U.S. politicians to fix underlying budget problems in the world's biggest economy.

"It's just show business, to distract from real issues and keep the public busy with nonsense," said Hennecke. "What they should negotiate is how to make a bankruptcy negotiation of the United States, because they are broke. That's the issue. It's not about some stupid debt ceiling."

China and Japan, which each own more than $1 trillion of Treasury securities, appealed earlier to Washington for a quick settlement. There was no indication whether either government had altered its debt holdings. South Korea's government has $51.4 billion of Treasury securities while Taiwan has $185 billion.

In Israel, a key American ally in the Middle East, commentators said the fight hurt America's overall image.

"There is no doubt that damage was done here to the image of American economic stability," Israel's economic envoy to Washington, Eli Groner, told Israel's Army Radio. "It's not good for the financial markets, not in the United States and not around the world."

China and other central banks might want to move assets into other currencies, said Hennecke. However, he said their dollar-based holdings are so huge they cannot sell without driving down prices.

[Associated

Press; By JOE McDONALD]

AP Business Writers

Kelvin Chan in Hong Kong, Youkyung Lee in Seoul and Kay Johnson in

Mumbai and AP Writers Peter Enav in Taipei, Tim Sullivan in New

Delhi and Tia Goldenberg in Jerusalem contributed.

Copyright 2013 The Associated

Press. All rights reserved. This material may not be published,

broadcast, rewritten or redistributed.

|