|

The U.S. Department of Justice last week alleged that the hedge fund

improperly classified two company investments as passive - and

therefore exempt from disclosure requirements - while taking an

activist role with executives. ValueAct disputes the claim. The U.S. Department of Justice last week alleged that the hedge fund

improperly classified two company investments as passive - and

therefore exempt from disclosure requirements - while taking an

activist role with executives. ValueAct disputes the claim.

Some communications the government cites as evidence are similar to

discussions that are increasingly common between traditional,

buy-and-hold funds and companies in their portfolios.

The case comes as active and passive investors work more together to

pressure management at underperforming companies. Activists court

passive shareholders before launching such a campaign, and passive

investors recruit activists to agitate, several activist managers

told Reuters.

Traditional funds may need to reassess their compliance with

disclosure laws, according to a memo to clients from Davis Polk, a

New York law firm with expertise in financial services.

"Such an institution will have to examine whether it can claim to

have a truly 'passive' intent," said the memo, issued in response to

the ValueAct case.

Those firms could include, for instance, T. Rowe Price Group <TROW.O>,

BlackRock Inc <BLK.N> and Vanguard Group. Spokespeople at those

companies declined to comment, and representatives of seven

additional fund firms contacted by Reuters declined to comment or

said executives were unavailable. The Justice Department also

declined to comment.

An industry trade group said the case could restrain shareholders

from addressing important issues with corporate executives and board

directors.

"The DOJ case could have a chilling effect on dialogues between

companies and their shareholders," said Amy Borrus, deputy director

at the Council of Institutional Investors, a Washington D.C.-based

nonprofit whose members include pensions, endowments and major

mutual funds.

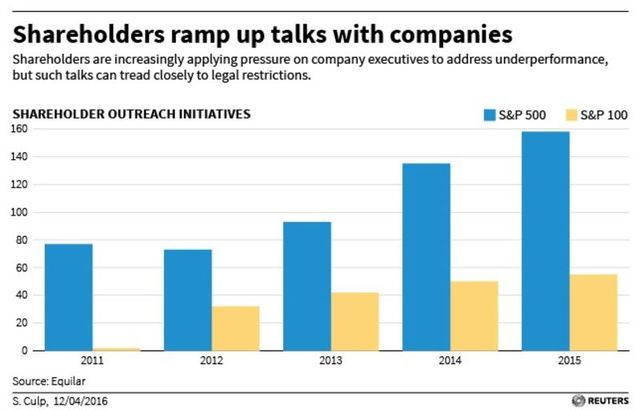

For a graphic showing the increase in company shareholder

communication programs, see http://tmsnrt.rs/25PYHpm

Competition for better returns has led some big mutual fund firms to

take a more active role, weighing in on issues such as CEO pay and

corporate governance. Vanguard Chairman and CEO William McNabb, in a

speech last June in New York, described how the firm increasingly

addresses matters of concern with companies in its portfolio.

"We’ve become more targeted in whom we mailed letters to and more

prescriptive in our language," McNabb said.

For example, Vanguard sent out 500 letters in March 2015 to

independent chairs and lead directors outlining six principles of

corporate governance, McNabb said.

SIX WORDS

At the heart of the ValueAct case are six words in a 40-year-old law

that requires disclosure of certain investments to assist the

Department of Justice and the Federal Trade Commission in antitrust

review of mergers. The intent is to prevent investors from secretly

buying up stakes to agitate for industry consolidation.

The Hart-Scott-Rodino Act requires all buyers of voting securities

worth more than $76.3 million to notify the government, unless they

were bought "solely for the purpose of investment."

The government alleges ValueAct failed to disclose a $2.5 billion

position in two companies that planned to merge - oilfield services

peers Halliburton Co and Baker Hughes Industries Inc.

[to top of second column] |

ValueAct is fighting the case and has said that its outreach to the

companies was standard shareholder input and not active investing.

The firm declined to comment for this story.

Among the evidence asserted by the government is a December 2014

meeting with the Baker Hughes chief financial officer, where

ValueAct’s chief executive discussed gaps in the company's North

American margins and other underperforming areas. The government

also cited a ValueAct email sent to Halliburton’s CEO in July 2015

to schedule a meeting about executive compensation.

Davis Polk points out in its client memo that it’s common for

investors with stakes deemed passive to discuss those topics with

corporate management.

"It does seem to be ... a typical subject of discussion," wrote the

firm, which represents Baker Hughes in the merger.

BLURRED BOUNDARIES

John Briggs, an antitrust attorney with the law firm Axinn, Veltrop

& Harkrider LLP, called the case a one-off enforcement effort

against ValueAct that does not necessarily signal a broader

crackdown or a change in legal interpretation.

But Briggs agreed that the case highlights the blurring boundaries

between activist and traditional fund managers. A ValueAct win could

further cloud the issue, while a government victory could prompt

major investors to dial back pressure on companies.

A managing director at a large asset manager, speaking on condition

of anonymity, said that he and his colleagues routinely discuss

business improvement and executive compensation with company

executives, believing such topics do not cross legal lines. The

ValueAct case could change that interpretation, the manager said.

The lawsuit could take months or years to resolve. Any resulting

limits on fund managers could clash with a separate effort led by

the U.S. Securities and Exchange Commission in the early 1990s

encouraging more dialogue between investors and public corporations.

"The idea was that you want to free up those conversations, since

more conversations allow more accountability," said University of

Delaware finance professor Charles Elson, who follows corporate

governance. "Anything that pushes things in a different direction is

problematic."

(Additional reporting by Diane Bartz in Washington)

[© 2016 Thomson Reuters. All rights

reserved.] Copyright 2016 Reuters. All rights reserved. This material may not be published,

broadcast, rewritten or redistributed. |