Powell faces early reckoning on Fed's $4-trillion

question

Send a link to a friend

Send a link to a friend

[January 29, 2019]

By Jonathan Spicer and Ann Saphir [January 29, 2019]

By Jonathan Spicer and Ann Saphir

NEW YORK/SAN FRANCISCO (Reuters) - Federal Reserve Chairman Jerome

Powell has a problem: how to explain that the Fed may soon begin to

taper its ongoing asset-shedding operation without looking like he's

hunkering down for a coming recession, or caving to U.S. President

Donald Trump.

Not long ago, Powell expected to face this delicate communication test

some time later in 2019, rather than at his news conference on Wednesday

following the close of the Fed's first policy meeting of the year.

But three things - an unexpected scarcity of reserves deep in the

plumbing of Wall Street, overt public pressure from investors and the

White House, and the Fed's own decision to rethink its interest-rate

hikes - are forcing the U.S. central bank to acknowledge the real

possibility of hanging on to more bonds than originally planned.

"You cannot stop the rate-hiking cycle without communicating on the

balance sheet as well," said Thomas Costerg, senior U.S. economist at

Pictet Wealth Management, in Geneva, Switzerland.

A bigger balance sheet could result in an across-the-board easing of

market borrowing costs and the foreign-exchange value of the dollar,

easing strains on emerging markets. It could also affect the Fed's

appetite for bond buying in the face of a future U.S. downturn.

For more than a year, the Fed has methodically trimmed its

multi-trillion-dollar balance sheet - from nearly $4.5 trillion to about

$4.1 trillion and falling - without much notice.

Instead, it has kept the world's eyes trained on a series of

interest-rate hikes which, according to careful messaging from

policymakers in recent weeks, may have come to an end.

But late last year, prominent investors took to blaming the Fed's

balance sheet runoff for market volatility. To underline what they saw

as the harmful restraining effects of the Fed's reversal of its

bond-buying stimulus, the program known as quantitative easing

undertaken during the financial crisis to jump-start the economy, they

dubbed the runoff "quantitative tightening."

In December, Trump amplified that theme, tweeting that the central bank

ought not to "make yet another mistake" and "stop with the 50 B's" - a

reference to the $50 billion maximum in bonds by which the Fed has been

shrinking its portfolio each month, according to a plan it outlined and

began in 2017.

A day after the tweet, when Powell said the run-off remained on

"automatic pilot," the Standard & Poor's 500 stock index delivered its

worst 60-minute selloff in at least a year.

Two weeks later, when Powell stressed that the plan was actually

flexible, the index delivered its best 60 minutes in at least a year.

Trump's tweet exposed a dilemma for the Fed: though its 2017 plan

divorced balance sheet policy from monetary policy, markets see a

stronger connection. If the Fed is to stick to its guns on keeping the

balance sheet from becoming a first-responder tool against economic ups

and downs, Powell needs to keep that divorce on the books.

"I don't think they're going to stop," said Chuck Self, chief investment

officer at iSectors LLC, in Appleton, Wisconsin. "They want to get it

down as low as they can without disrupting the economy."

[to top of second column] |

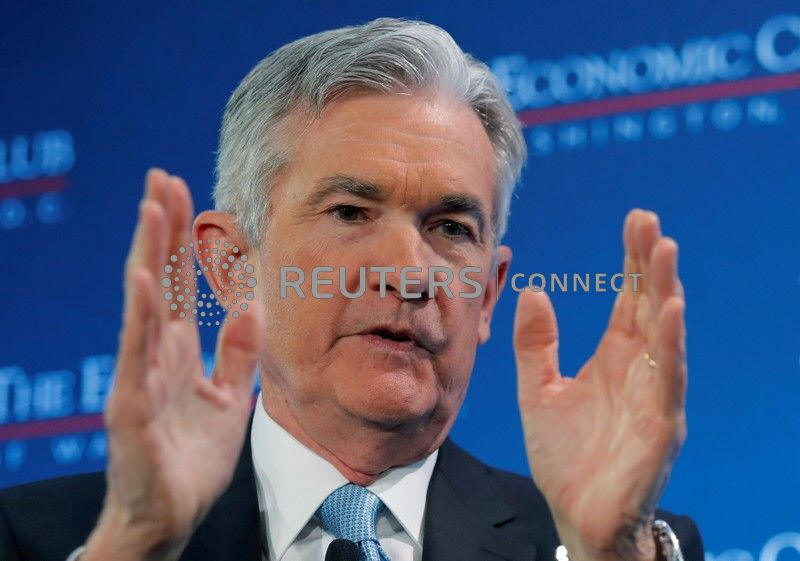

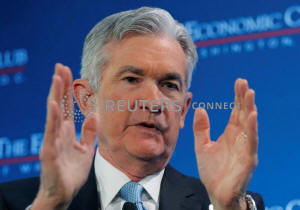

U.S. Federal Reserve

Board Chairman Jerome Powell participates in a luncheon discussion

hosted by the Economic Club in Washington, U.S., January 10, 2019.

REUTERS/Jim Young/File Photo

A CLEARER ROAD MAP

The central bank is indeed nearing the point at which it needs to adjust its

balance sheet plan, not because of the state of the domestic economy, which

appears strong, but because of the plumbing of short-term markets.

As the portfolio has decreased, banks have trimmed the reserves they keep at the

Fed by even greater amounts, putting a strain on the Fed's ability to control

the short-term policy rate by which it steers monetary policy.

(GRAPHIC: Bank excess reserves held at the Fed - https://tmsnrt.rs/2BiDDzx)

Economists had already speculated last summer that to deal with mounting

scarcity of reserves, and the resulting upward push on interest rates beyond a

target range, the run-off would need to end two years earlier and leave the Fed

with $1 trillion more than it had envisioned.

For its part, the Fed aims to trim its portfolio to an unspecified level at

which demand for reserves matches supply - though not to as low as the $900

billion it held before the 2007-2009 recession prompted it begin the purchases.

"It'll be substantially smaller than it is now...but nowhere near where it was

before," Powell said on Jan. 10, framing any decision as a technical one and not

a referendum on the overall policy stance.

Growing questions about the balance sheet may prompt Powell to sketch out a

clearer road map for the asset holdings at his 2:30 p.m. (19:30 GMT) Wednesday

news conference.

"They've got to get started on that," Darrell Duffie, a professor at Stanford

University's graduate school of business, said of telegraphing the policy

change. "They are not boxed in now, but the longer they wait, the more boxed in

they'll be."

After raising rates gradually last year, the Fed is taking a wait-and-see

approach to further tightening in the face of an overseas slowdown and market

volatility.

But even if rates remain steady this year, the ongoing shedding of assets,

including some $380 billion since October 2017, will continue to tighten

financial conditions by making funding more expensive for banks.

In 2017, the Fed projected it would trim the portfolio until around 2022 when it

would hold $2.3 trillion to $2.9 trillion in assets.

But minutes from the Fed's December meeting showed growing internal debate with

policymakers mulling holding a larger "buffer" of securities than planned, or

slowing the pace of run-off as the finish line approaches.

In mid-2018, economists at Deutsch Bank Securities were among those predicting

the Fed would be forced to stop the process by early 2020 with about $3.7

trillion in assets.

The minutes, they wrote in a note, have "shifted the balance of risks" even more

and convinced them that Powell will move to halt the portfolio run-off as early

as the third quarter of 2019.

In a possible preview of Powell's message, New York Fed President John Williams,

a permanent voter on the Fed's policy-setting committee, said on Jan. 18: "If

circumstances change, I will reassess our choices regarding monetary policy,

including the path of balance sheet normalization. Data dependence applies to

all that we do."

(Reporting by Jonathan Spicer and Ann Saphir; Additional reporting by Trevor

Hunnicutt; Editing by Leslie Adler)

[© 2019 Thomson Reuters. All rights

reserved.] Copyright 2019 Reuters. All rights reserved. This material may not be published,

broadcast, rewritten or redistributed.

Thompson Reuters is solely responsible for this content. |