As Fed nears rate cut, policymakers debate how deep, and even if

Send a link to a friend

Send a link to a friend

[July 17, 2019] By

Howard Schneider [July 17, 2019] By

Howard Schneider

CHICAGO (Reuters) - With the first U.S.

interest rate reduction in a decade expected later this month, two

Federal Reserve policymakers sketched out arguments on Tuesday on how

deep the cut should be, even as a third said she needs more data before

being ready to sign on at all.

The remarks, from the chiefs of the Federal Reserve regional banks of

Chicago, Dallas and San Francisco, show that the U.S. central bank is

edging toward a widely anticipated rate cut at its upcoming July 30-31

meeting without a consensus narrative about why a cut is needed, or even

if it is.

The competing cases made Tuesday by the two policymakers supportive of a

rate cut suggested the decision of whether to reduce rates by a quarter

or a half of a percentage point could hinge on whether the goal is to

guard against developing risks in the world economy and signaled by bond

markets, or deliver a solid jolt meant to boost inflation in the United

States.

"There is an argument that if I think it takes 50 basis points before

the end of the year to get inflation up, then something right away would

make that happen sooner," Chicago Fed President Charles Evans told

reporters at a CNBC economic forum.

Evans last week said he felt a reduction of half a percentage point in

the Fed's target overnight interest rate was needed for the U.S. central

bank to deliver on the 2% inflation target that it has missed since

setting it in 2012.

The Fed set the goal as a way to keep businesses and households forward

looking, and help assure a modest pace of price and wage increases.

Evans and others are concerned that if they continue to undershoot, they

will lose credibility and their statements and policies will become less

effective.

The Fed's current policy interest rate is set in a range of between

2.25% and 2.5%.

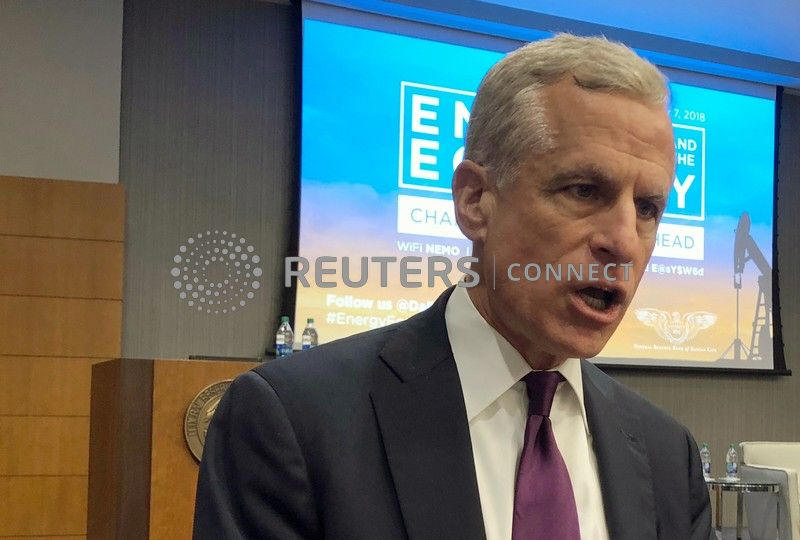

By contrast, Dallas Fed President Robert Kaplan, until recently a

skeptic that rates should be cut at all, said he now thinks a "tactical"

reduction of a quarter point could address the risks apparently seen by

bond investors, who have pushed some long-term yields below shorter-term

ones.

"If it was appropriate to take action, the best argument for me of why

to do that is the shape of the curve," Kaplan told reporters in

Washington, referring to the "inversion" of the bond yield curve, a

standard warning sign of recession.

The bond yield curve, when plotted as a graph, inverts from its typical

arcing, upward slope when shorter-dated yields exceed those of

longer-duration securities.

[to top of second column] |

Dallas Federal Reserve Bank President Robert Kaplan speaks with an

attendee at an annual energy conference at the Dallas Fed

headquarters in Dallas, Texas, U.S. September 7, 2018. REUTERS/Ann

Saphir

But neither the inversion of the yield curve nor concern about muted inflation

or headwinds that may slow economic growth was enough to convince San Francisco

Fed Bank President Mary Daly yet of the need to ease policy.

"At this point I'm not leaning one direction or another," Daly told Reuters in

an interview, when asked about the Fed's July rate decision.

The economy needs to grow above its trend annual pace of 2% to get inflation

back to the Fed's 2% goal, she said. "The question in my mind is, Does the

economy have that on its own, or will additional stimulus be needed to get it

there? And it's too early to tell," she said.

Policymakers have cited international risks, the uncertainty of President Donald

Trump's trade policies, the pricing in bond markets and weak inflation, among

other factors, as cause to cut interest rates even though the economy is growing

and unemployment is at a record low.

Fed Chairman Jerome Powell, speaking in Paris on Tuesday, reiterated a pledge to

"act as appropriate" to keep the U.S. economy humming. But even with the economy

continuing to turn in "solid" growth that is helping to keep a "strong labor

market," Powell said with inflation falling short of the Fed's target and a

basket of "uncertainties," it is harder to remain confident in a still-rosy

outlook.

Evans said on Tuesday that each policymaker's decision on how much to cut may

well be shaped by that person's argument for why to do it.

While higher inflation may require the shock of a deeper cut, he said, "for

those who are thinking this is more risk management - a strong domestic economy

facing some uncertainty - you could easily argue to go a little slower."

(Reporting by Howard Schneider; Additional reporting by Trevor Hunnicutt, Jason

Lange and Ann Saphir; Editing by Leslie Adler)

[© 2019 Thomson Reuters. All rights

reserved.] Copyright 2019 Reuters. All rights reserved. This material may not be published,

broadcast, rewritten or redistributed.

Thompson Reuters is solely responsible for this content.

|