Fed will be tested in 2021 as vaccines boost U.S.

economic outlook

Send a link to a friend

Send a link to a friend

[December 15, 2020] By

Ann Saphir [December 15, 2020] By

Ann Saphir

(Reuters) - If 2020 was the year the

Federal Reserve overhauled its game plan for supporting the U.S.

economy, 2021 will be the year its new approach gets tested should a

coronavirus vaccine deliver the lift that many analysts expect.

In its final policy meeting of the year this week, the U.S. central bank

is expected to keep its key overnight interest rate pinned near zero and

to signal it will stay there for years to come; many analysts also

expect new guidance on how long the Fed will keep up its massive

bond-buying program.

The super-easy monetary policy is part of a long-term strategy the Fed

adopted in August to help it navigate a world of persistently low

interest rates that limits the central bank's options for fighting

downturns and makes it difficult to hit its 2% inflation goal.

The idea is to counteract any unhealthy downward drag on prices by

letting the economy run hotter than in the past. The Fed now plans to

keep rates near zero until the economy reaches full employment and

inflation hits 2% and is on track to exceed it.

Re-upping that bold promise this week won't seem out of place amid the

alarming U.S. rise in COVID-19 cases and deaths that threatens to stall

a still-partial recovery. The labor market has regenerated only about

half of the 22 million jobs lost since the pandemic began.

But next year, when a full rollout of new coronavirus vaccines is

expected to make it gradually safer to dine out, travel, and resume

other activities put on hold during the crisis, the Fed's new framework

will be tested.

Economic growth is expected to pick up, and job gains with it, both

views that are likely to be reflected in fresh economic projections

released after the Fed wraps up its two-day meeting on Wednesday.

But the central bank's so-called "dot plot" of interest rate

expectations, included in those projections, will likely show most

policymakers still see rates at zero through 2023.

That's consistent with the new framework if the economy hasn't achieved

sustained 2% inflation by then.

But Aneta Markowska, chief financial economist at Jefferies, said it

"would be nice (for the Fed) to demonstrate what happens to the reaction

function after inflation reaches 2%."

[to top of second column] |

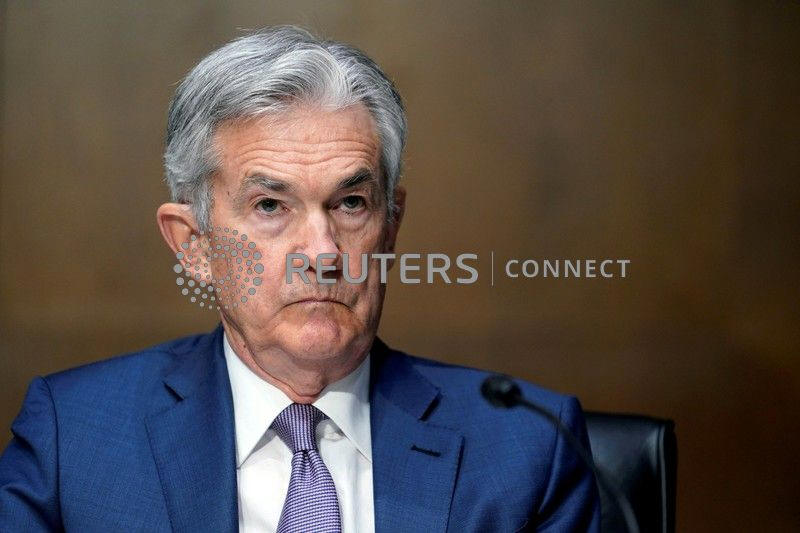

Federal Reserve Chairman Jerome Powell testifies before the Senate

Banking Committee hearing on "The Quarterly CARES Act Report to

Congress" on Capitol Hill in Washington, U.S., December 1, 2020.

Susan Walsh/Pool via REUTERS/File Photo

'PLAYING THE LONG GAME'

The first opportunity could come in the spring.

A sharp increase in demand as COVID-19 inoculations allow more of the economy to

reopen could push inflation above the Fed's 2% target, at least for a time, says

Andrew Hunter, senior U.S. economist at Capital Economics.

At that point, "the Fed may have to take slightly clearer steps to emphasize

that they are not going to raise rates," Hunter said.

Or, as Chicago Fed President Charles Evans has explained it, the Fed will need

to show it is "in it to win it." Exactly what that means will depend on the

circumstances.

If markets push up long-run interest rates a bit to reflect expectations for

future faster growth, the Fed likely wouldn't change course.

The problem, said AllianceBernstein senior economist Eric Winograd, is that "the

market may be tempted to look at a cyclical upswing ... and conclude that the

Fed will respond as it always has, by starting to tighten."

If traders begin pricing in earlier rate hikes, the Fed would need to react,

either by correcting the market's misperception verbally or, if needed, by

tweaking its bond-buying program to push down further on longer-term borrowing

costs through purchases of longer-term securities.

If the Fed issues new guidance on its asset purchase program this week, it may

need to leave the door open to doing exactly that, in part as insurance against

any market overreaction to an improving economic outlook next year.

"The Fed is playing the long game," Winograd said.

(Reporting by Ann Saphir; Editing by Dan Burns and Paul Simao)

[© 2020 Thomson Reuters. All rights

reserved.] Copyright 2020 Reuters. All rights reserved. This material may not be published,

broadcast, rewritten or redistributed.

Thompson Reuters is solely responsible for this content. |