Bubbles, bubbles everywhere: Jeremy Grantham on the bust ahead

Send a link to a friend

Send a link to a friend

[July 20, 2021] By

Chris Taylor [July 20, 2021] By

Chris Taylor

NEW YORK (Reuters) - In this manic era of

meme stocks, cryptocurrencies and real-estate bidding wars, studying the

history of financial markets might seem a little dry and old-fashioned.

Except to Jeremy Grantham.

The chairman of the board of famed asset managers GMO is a certified

bubble-ologist, fascinated by how and why bubbles emerge. Grantham

studies classic ones like 1929, but - now in his eighties - he has also

lived through (and called) numerous modern booms and busts, including

the dot-com wreckage in 2000, the bull market peak in 2008 and the bear

market low in 2009.

In case you did not know where this is headed: He says we are in a

bubble right now.

In January Grantham wrote an investor letter, "Waiting For the Last

Dance," about an inflating bubble that "could well be the most important

event of your investing lives."

Six months later, the stock market is starting to show some cracks.

Grantham spoke with Reuters about this moment of market history.

Q: When your letter of warning came out, what was the response like?

A: I got a lot of pushback. Waves of Bitcoin freaks attacked me in every

way possible. They said my ears were too big, and that I needed to be

locked up in an old-folks home.

Q: So if we were already in a bubble then, where do things stand right

now?

A: Bubbles are unbelievably easy to see; it's knowing when the bust will

come that is trickier. You see it when the markets are on the front

pages instead of the financial pages, when the news is full of stories

of people getting cheated, when new coins are being created every month.

The scale of these things is so much bigger than in 1929 or in 2000.

Q: What is your take on equity valuations now?

A: Looking at most measures, the market is more expensive than in 2000,

which was more expensive than anything that preceded it.

My favorite metric is price-to-sales: What you find is that even the

cheapest parts of the market are way more expensive than in 2000.

Q: What might bring an end to this bubble?

A: Markets peak when you are as happy as you can get, and a near-perfect

economy is extrapolated into the indefinite future. But around the

corner are lurking serious issues like interest rates, inflation, labor

and commodity prices. All of those are beginning to look less optimistic

than they did just a week or two ago.

Q: How long until a bust?

[to top of second column] |

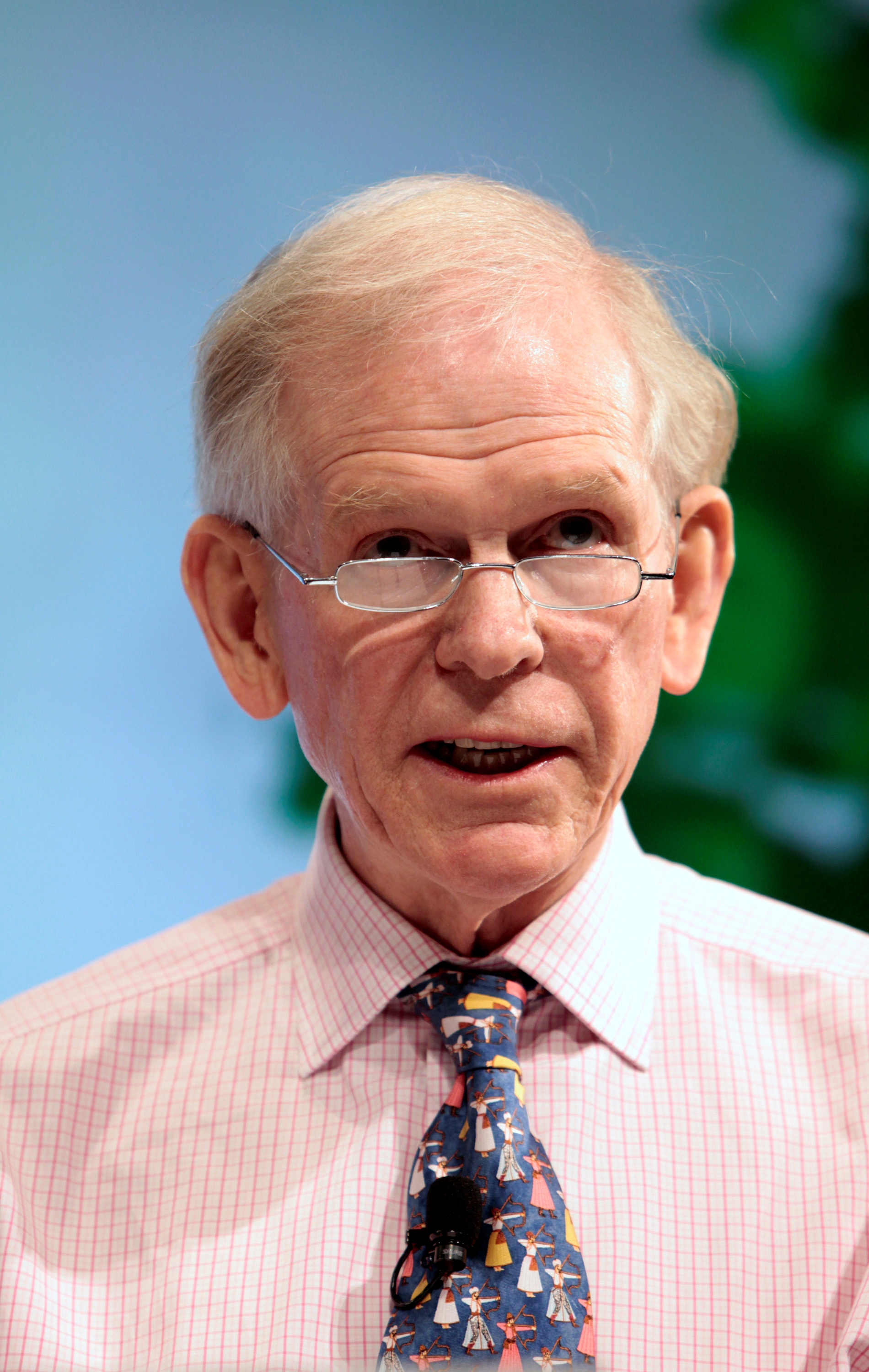

Jeremy Grantham, Co-founder and Chief Investment Strategist of GMO,

speaks on financial innovation at Pace University in New York

October 16, 2009. REUTERS/Nicholas Roberts/File Photo

A: A bust might take a few more months, and, in fact, I hope it does, because it

will give us the opportunity to warn more people. The probabilities are that

this will go into the fall: The stimulus, the economic recovery, and

vaccinations have all allowed this thing to go on a few months longer than I

would have initially guessed.

What pricks the bubble could be a virus problem, it could be an inflation

problem, or it could be the most important category of all, which is everything

else that is unexpected. One of 20 different things that you haven't even

thought of will come out of the woodwork, and you had no idea it was even there.

Q: What might a bust look like?

A: There will be an enormous negative wealth effect, broader than it has ever

been, compared to any other previous bubble breaking. It's the first time we

have bubbled in so many different areas – interest rates, stocks, housing,

non-energy commodities. On the way up, it gave us all a positive wealth effect,

and on the way down it will retract, painfully.

Q: Are there any asset classes which are relatively attractive?

A: You could always own cash, or you could do what the institutions do, which is

buy heavily into the asset classes that are least bad. The least overpriced are

value stocks and emerging markets. Those are the two arbitrages. With value and

emerging, you should make some positive return over the next 10 years.

Q: It is difficult to be bearish right now?

A: Not for me, because I don't have career risk anymore. But every big company

has lots of risk: They facilitate a bubble until it bursts, and then they change

their tune as fast as they can, and make money on the downside.

But this bubble is the real thing, and everyone can see it. It's as obvious as

the nose on your face.

(Reporting by Chris Taylor; editing by Lauren Young and Richard Pullin; Follow

us @ReutersMoney or at http://www.reuters.com/finance/personal-finance.)

[© 2021 Thomson Reuters. All rights

reserved.] Copyright 2021 Reuters. All rights reserved. This material may not be published,

broadcast, rewritten or redistributed.

Thompson Reuters is solely responsible for this content. |