Illinois Supreme Court strikes down Cook County tax on guns

Send a link to a friend

Send a link to a friend

[October 22, 2021]

By JERRY NOWICKI

Capitol News Illinois

jnowicki@capitolnewsillinois.com

SPRINGFIELD – The Illinois Supreme Court

ruled Thursday that a Cook County tax on gun purchases is

unconstitutional, but it left the door open for a more tailored tax that

specifically goes toward mitigating gun violence and its effects. SPRINGFIELD – The Illinois Supreme Court

ruled Thursday that a Cook County tax on gun purchases is

unconstitutional, but it left the door open for a more tailored tax that

specifically goes toward mitigating gun violence and its effects.

The Cook County gun tax, which took effect in April 2013, imposed a $25

fee for retail gun purchases in the county, as well as a 5 cent fee per

cartridge of centerfire ammunition and 1 cent per cartridge fee for

rimfire ammunition.

The taxes were challenged by the trade group Guns Save Life Inc. in a

lawsuit against the county.

The Supreme Court’s Thursday opinion, written by Justice Mary Jane

Theis, stated that, “While the taxes do not directly burden a

law-abiding citizen’s right to use a firearm for self-defense, they do

directly burden a law-abiding citizen’s right to acquire a firearm and

the necessary ammunition for self-defense.”

In the 14-page, 6-0 opinion, the Supreme Court reversed an appellate

court ruling that would have allowed the taxes to stay in place. Chief

Justice Anne Burke did not take part in the decision.

While the court rejected the tax, it did specifically note that the

county’s failure to earmark the revenue from the tax for gun violence

prevention programs played a major role in the decision.

It gave particular scrutiny to the question of whether the tax violated

the uniformity clause of the Illinois Constitution, which states: “In

any law classifying the subjects or objects of non-property taxes or

fees, the classes shall be reasonable and the subjects and objects

within each class shall be taxed uniformly.”

Citing previous court precedent related to that clause, the court wrote

it had to determine whether the tax on guns “bears some reasonable

relationship to the object of the legislation or to public policy.”

“Under the plain language of the ordinances, the revenue generated from

the firearm tax is not directed to any fund or program specifically

related to curbing the cost of gun violence,” the court wrote.

“Additionally, nothing in the ordinance indicates that the proceeds

generated from the ammunition tax must be specifically directed to

initiatives aimed at reducing gun violence. Thus, we hold the tax

ordinances are unconstitutional under the uniformity clause.”

Justice Michael Burke agreed with the opinion, but issued a four-page

special concurrence disagreeing with the majority’s analysis that the

county’s spending plans affected whether the tax was permissible.

“The majority’s analysis is problematic because it leaves space for a

municipality to enact a future tax — singling out guns and ammunition

sales — that is more narrowly tailored to the purpose of ameliorating

gun violence,” Michael Burke wrote.

[to top of second column]

|

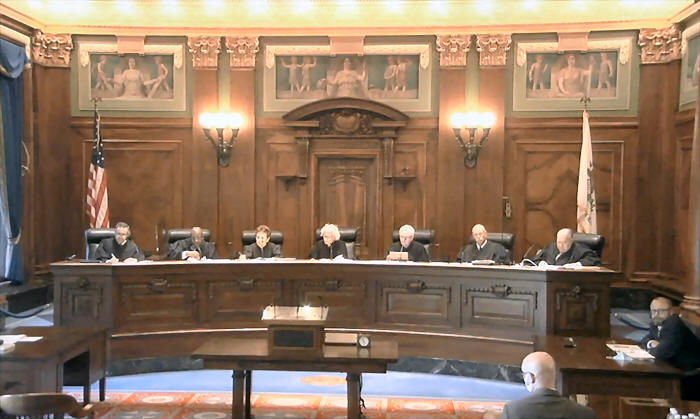

The Illinois Supreme Court is pictured at the Supreme

Court building in Springfield last month. The justices struck down a

Cook County tax on gun sales in an opinion released Thursday.

(Credit: Blueroomstream.com)

He argued the majority opinion is leading the county

“down a road of futility,” citing Article 1, Section 22 of the state

constitution, which reads: “Subject only to the police power, the

right of the individual citizen to keep and bear arms shall not be

infringed.”

“The only problem with the majority’s approach — and the guidance it

offers the county — is that such counsel, if followed, would still

violate the provision of the Illinois Constitution noted above that

plainly states that the right of the individual to keep and bear

arms is subject only to the police power, not the power to tax,” he

wrote.

“Thus, the majority is leading the county down a road of futility,”

he added.

One major precedent cited by the court was from Boynton vs. Kusper,

a 1986 Supreme Court ruling which struck down a $10 state tax on

marriage licenses in certain counties that went to the Domestic

Violence Shelter and Services fund.

The court said at the time the marriage license tax “directly

impeded the exercise of the fundamental right to marry,” and should

be subject to greater scrutiny.

The court ruled in the Boynton case that even though the $10 fee was

“de minimis,” or small, if the court granted that authority, it

would essentially mean “there is no limit on the amount of the tax

that may be imposed,” according to previous case law.

The same argument can be applied to the gun tax, the court wrote,

noting that a stricter level of scrutiny is needed because the tax

applies to a fundamental right.

Given that necessary scrutiny, the court ruled the gun taxes

unconstitutional.

“In applying that standard to the firearm and ammunition taxes, we

recognize that the uniformity clause was ‘not designed as a

straitjacket’ for the county … and acknowledge the costs that gun

violence imposes on society,” the court wrote. “Nevertheless, the

relationship between the tax classification and the use of the tax

proceeds is not sufficiently tied to the stated objective of

ameliorating those costs.”

Capitol News Illinois is a nonprofit, nonpartisan

news service covering state government and distributed to more than

400 newspapers statewide. It is funded primarily by the Illinois

Press Foundation and the Robert R. McCormick Foundation. |