Marketmind: Powell's feint

Send a link to a friend

Send a link to a friend

[August 26, 2022] A

look at the day ahead in U.S. and global markets from Mike Dolan. [August 26, 2022] A

look at the day ahead in U.S. and global markets from Mike Dolan.

With just four hours to Jerome Powell's podium appearance at Jackson

Hole, all the 'ifs' and 'buts' have been debated and the jerky last

minute market positioning done and dusted.

The only worry left is that it might be a damp squib.

The Federal Reserve chief delivers his hotly-awaited speech at 1000 EDT.

(1400 GMT)

But the barrage of comments and interviews from his Fed colleagues over

the past 24 hours leaves markets with little new to chew on about the

policy trajectory.

Interest rate futures go into the setpiece with a much more hawkish bias

compared to early August, putting the Fed's peak 'terminal' rate early

next year at about 3.8%. Yet that's still below the 4% peak they

expected in mid June and there's still at least one rate cut penciled in

from there to the end of 2023.

Powell's unlikely to be specific about next month's decision, preferring

to wait for critical jobs and inflation data out before then. An easing

in July of the Fed's preferred inflation measure - the core personal

consumption expenditure index - will likely be seen before he speaks

later.

That said, futures are again leaning to 60% chance of another 75 basis

point hike at the September meeting.

One possible focus is that Powell avoids detailed guidance on 'peak

rates' but emphasises that they are unlikely to be cut next year at all.

Any finer points on the Fed' balance sheet rundown will also be lapped

up, with some analysts now fearful that standing assumptions on the pace

of so-called 'quantitative tightening' could drain commercial bank

reserves too fast into any sharp slowdown next year.

Even though bond markets wobbled and the dollar jumped back in

anticipation of the speech this week, Wall St stocks seemed less

bothered - staging their best one-day rally in two weeks on Thursday and

with stock futures holding those gains today.

[to top of second column] |

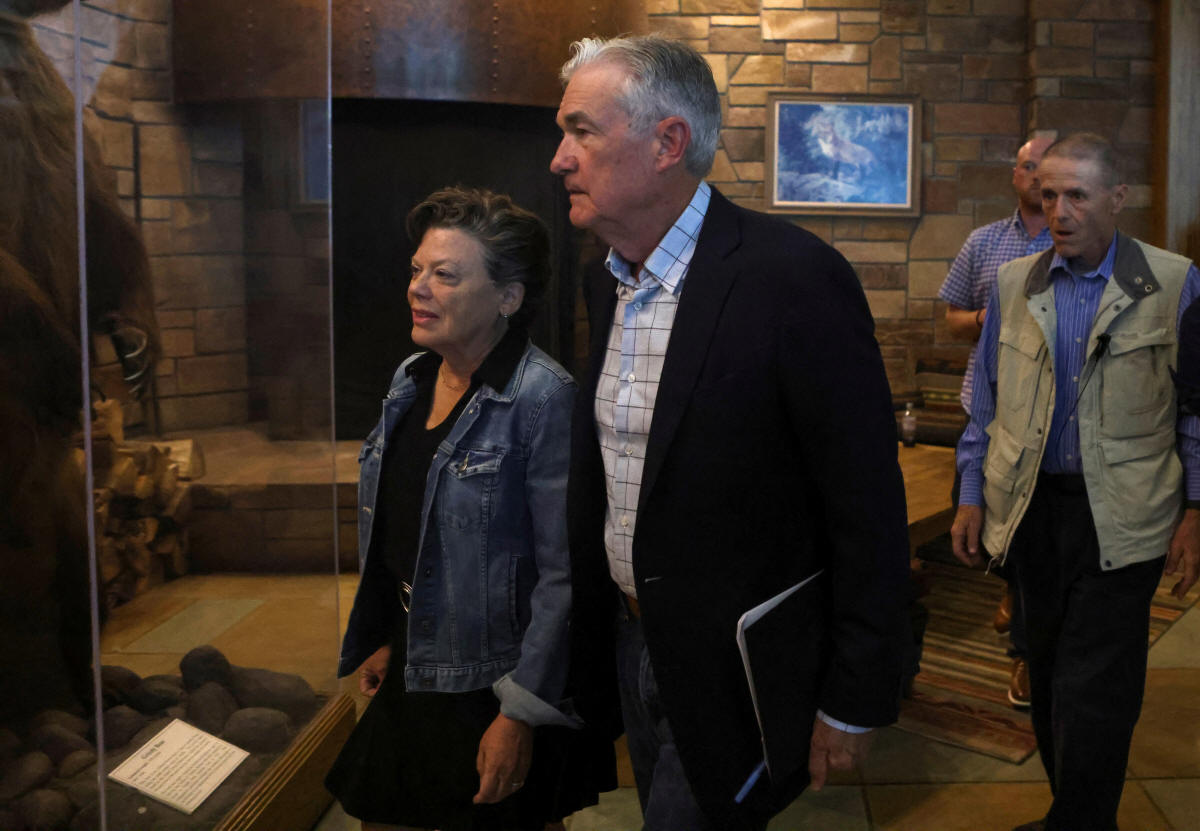

Jerome Powell, chair of the Federal

Reserve, and his wife Elissa Leonard attend a dinner program at

Grand Teton National Park where financial leaders from around the

world are gathering for the Jackson Hole Economic Symposium outside

Jackson, Wyoming, U.S., August 25, 2022. REUTERS/Jim Urquhart

While Bank of America's weekly investment flows tally shows a further exit from

most asset classes and overall positioning still at 'maximum bearish', financial

stocks stood out this week with their biggest inflow since January.

Powell aside, world markets were focussed on Friday on the deepening European

energy crunch and China's latest stimulus plans on infrastructure spending.

Copper prices hit their highest in two weeks on the latter.

But it's set to be a cold winter. Describing it as a bone fide 'crisis', British

regulators announced that household energy bills will rise 80% a year from

October. Soaring energy bills also pushed Germany's consumer confidence reading

to record low for third month in a row.

Brent crude oil prices, so crucial to the inflation and central bank narrative

this year, held this week's gains back to $100 per barrel - largely on fears

OPEC will cut output if a nuclear deal ushers Iranian crude back to world

markets.

Key developments that should provide more direction to U.S. markets later on

Friday:

* U.S. July personal consumption, Core PCE price index

* US July advance goods trade balance

* U.S. final August Michigan consumer sentiment index reading

* Fed chief Jerome Powell speaks at Jackson Hole 1400 GMT

(By Mike Dolan, editing by Kim Coghill mike.dolan@thomsonreuters.com. Twitter:

@reutersMikeD)

[© 2022 Thomson Reuters. All rights

reserved.]This material may not be published,

broadcast, rewritten or redistributed.

Thompson Reuters is solely responsible for this content. |