|

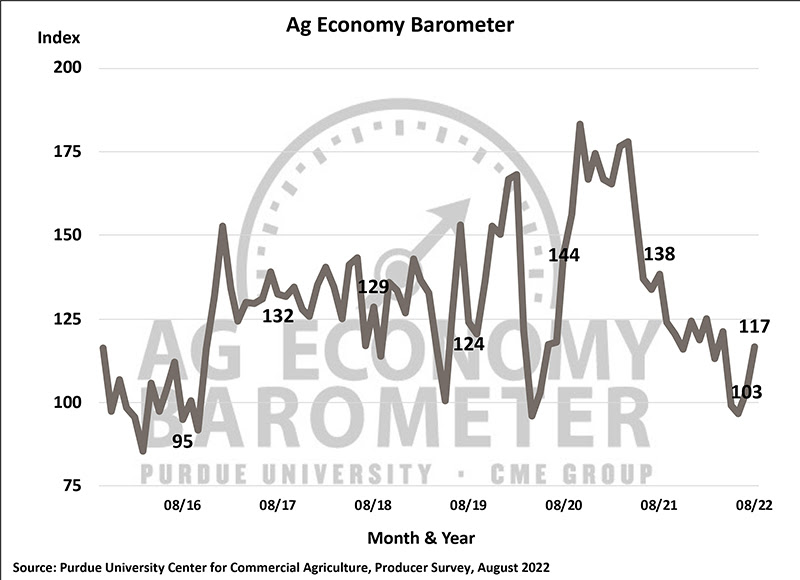

The rise in the overall measure of agricultural producer

sentiment was driven by increases in both the Index of Current

Conditions, which rose 9 points to 118, and the Index of Future

Expectations, which climbed 16 points to 116. The Ag Economy

Barometer is calculated each month from 400 U.S. agricultural

producers’ responses to a telephone survey. This month’s survey

was conducted Aug. 15-19, after The U.S. Department of

Agriculture released both the August Crop Production and World

Agricultural Supply and Demand Estimates reports. The rise in the overall measure of agricultural producer

sentiment was driven by increases in both the Index of Current

Conditions, which rose 9 points to 118, and the Index of Future

Expectations, which climbed 16 points to 116. The Ag Economy

Barometer is calculated each month from 400 U.S. agricultural

producers’ responses to a telephone survey. This month’s survey

was conducted Aug. 15-19, after The U.S. Department of

Agriculture released both the August Crop Production and World

Agricultural Supply and Demand Estimates reports.

“Producers in the August survey were less worried about their

farm’s financial situation than in July, although they remain

concerned about a possible cost/price squeeze,” said James

Mintert, the barometer’s principal investigator and director of

Purdue University’s Center for Commercial Agriculture.

This month, more producers indicated they’re expecting better

financial performance for their farms in 2022 and the upcoming

year, as the Farm Financial Performance Index improved 11 points

to a reading of 99. Both corn and soybean prices rallied from

their July lows into mid-August which, along with expectations

for good yields, helped explain some of the improvement in

financial performance expectations.

At the same time, there continues to be a tremendous amount of

uncertainty among producers regarding the future cost of items

they purchase both for their farms and family usage. When asked

about their biggest concerns for the next year, over half (53%)

of respondents chose higher input costs, followed by rising

interest rates (14%), input availability (12%), and lower output

prices (11%). On the farm level, there is a big disparity in

opinions among farmers regarding whether input prices will

retreat or escalate in 2023. Approximately four out of 10

producers expect crop input prices in 2023 to be either

unchanged or possibly decline by as much as 10%, compared to

2022. On the other hand, just over half of all producers expect

input prices to rise from 1% to 20%. At the consumer level,

nearly half (48%) of respondents said they expect the rate of

inflation for consumer items during the next 12 months to be in

the 0% to 6% range. Compared to previous barometer surveys, more

producers this month said they expect inflation to be in the

upper end of that range than those who felt that way earlier

this year.

Producers continue to view now as a bad time to make large farm

machinery and building investments. In a follow-up question,

nearly half (49%) of those who said it is a bad time for

investing cited increasing prices as the primary reason. The

Farm Capital Investment Index remains near its record low, but

was up 3 points to a reading of 39 in August.

Upward pressure on cash rental rates for Corn Belt farmland in

2023 seems likely. Four out of 10 corn and soybean producers

expect farmland cash rental rates to rise in 2023 compared to

2022. This month, 27% of respondents said they expect rates to

rise up to 5% compared to 39% of respondents who expect rates to

rise between 5% and 10% in 2023.

Expectations for both short- and long-term farmland values were

nearly unchanged over the previous month. Among survey

respondents who say they expect farmland values to rise over the

next five years, well over half (57%) chose nonfarm investor

demand as the main reason they expect values to rise.

To understand producers’ exposure to and

experiences with companies offering payments for capturing

carbon, this month’s survey asked respondents if they’ve engaged

in these types of discussions and the payments being offered. In

August, 9% of respondents said they have engaged in discussions

with companies offering payments for carbon capture, the highest

percentage of respondents since the question was first included

in the survey. Of those who engaged in discussions, 75% said the

payment rate per metric ton of carbon offered was less than $20,

and just 1% said they have signed a carbon contract. Respondents

who engaged in discussions and chose not to sign a contract were

asked the minimum payment per acre they would accept to enroll

their farm in a carbon capture program.

[to top of second column] |

Two-thirds of those respondents said the payment rate

needed to be at least $30 per acre, suggesting that payment rates

need to rise to encourage more participation in carbon capture

programs.

Read the full Ag Economy Barometer report. The site also offers

additional resources – such as past reports, charts and survey

methodology – and a form to sign up for monthly barometer email

updates and webinars.

Each month, the Purdue Center for Commercial Agriculture provides a

short video analysis of the barometer results. For even more

information, check out the Purdue Commercial AgCast podcast. It

includes a detailed breakdown of each month’s barometer, in addition

to a discussion of recent agricultural news that affects farmers.

The Ag Economy Barometer, Index of Current Conditions and Index of

Future Expectations are available on the Bloomberg Terminal under

the following ticker symbols: AGECBARO, AGECCURC and AGECFTEX.

About the Purdue University Center for Commercial Agriculture

The Center for Commercial Agriculture was founded in 2011 to provide

professional development and educational programs for farmers.

Housed within Purdue University’s Department of Agricultural

Economics, the center’s faculty and staff develop and execute

research and educational programs that address the different needs

of managing in today’s business environment.

About CME Group

As the world’s leading and most diverse derivatives marketplace, CME

Group (www.cmegroup.com) enables clients to trade futures, options,

cash and OTC markets, optimize portfolios, and analyze data –

empowering market participants worldwide to efficiently manage risk

and capture opportunities. CME Group exchanges offer the widest

range of global benchmark products across all major asset classes

based on interest rates, equity indexes, foreign exchange, energy,

agricultural products and metals. The company offers futures and

options on futures trading through the CME Globex® platform, fixed

income trading via BrokerTec and foreign exchange trading on the EBS

platform. In addition, it operates one of the world’s leading

central counterparty clearing providers, CME Clearing. With a range

of pre- and post-trade products and services underpinning the entire

lifecycle of a trade, CME Group also offers optimization and

reconciliation services through TriOptima, and trade processing

services through Traiana.

CME Group, the Globe logo, CME, Chicago Mercantile Exchange, Globex,

and E-mini are trademarks of Chicago Mercantile Exchange Inc. CBOT

and Chicago Board of Trade are trademarks of Board of Trade of the

City of Chicago, Inc. NYMEX, New York Mercantile Exchange and

ClearPort are trademarks of New York Mercantile Exchange, Inc. COMEX

is a trademark of Commodity Exchange, Inc. BrokerTec, EBS, TriOptima,

and Traiana are trademarks of BrokerTec Europe LTD, EBS Group LTD,

TriOptima AB, and Traiana, Inc., respectively. Dow Jones, Dow Jones

Industrial Average, S&P 500, and S&P are service and/or trademarks

of Dow Jones Trademark Holdings LLC, Standard & Poor’s Financial

Services LLC and S&P/Dow Jones Indices LLC, as the case may be, and

have been licensed for use by Chicago Mercantile Exchange Inc. All

other trademarks are the property of their respective owners.

[Writer: Kami Goodwin

Source: James Mintert]

|