Ex-Fed chief Bernanke says labor costs becoming more prominent in

inflation

Send a link to a friend

Send a link to a friend

[May 23, 2023] By

Howard Schneider [May 23, 2023] By

Howard Schneider

WASHINGTON (Reuters) - A tight U.S. job market and rising wages are

beginning to have more of an impact on inflation and could embed faster

rising prices if the demand for workers is not brought into better

balance with the labor force, new research from an ex-Federal Reserve

chief and a former top International Monetary Fund economist has

concluded.

Ben Bernanke, who led the U.S. central bank from 2006-2014, and Olivier

Blanchard, the IMF's chief economist from 2008 to 2015, said the

inflation surge starting in 2021 was largely stoked by energy markets

and shortages of automobiles and other durable goods.

"However, over time a very tight labor market has begun to exert

increasing pressure on inflation ... That share is likely to grow and

will not subside on its own," they wrote in a paper released on Tuesday

by the Washington-based Brookings Institution. "The portion of inflation

which traces its origin to overheating of labor markets can only be

reversed by policy actions that bring labor demand and supply into

better balance."

The U.S. central bank has raised interest rates aggressively since March

of 2022 to try to slow the economy and reduce the overall demand for

goods and services. While policymakers are expected, for now, to hold

off on another rate increase at their June 13-14 policy meeting, they

have remained noncommittal as they await upcoming inflation and jobs

data.

The paper adds a new set of arguments, from two influential economists

who witnessed inflation's broad retreat during their policymaking terms,

to one of the Fed's central debates: what role a looser job market and

slower wage growth will need to play in any continued lowering of

inflation from levels that remain high and are only slowly improving.

LABOR MARKET SLACK

Some Fed economists and policymakers feel a point of steady

"disinflation" may be close, and hinges only on families and businesses

spending final doses of pandemic-era cash. Others, most notably Chicago

Fed President Austan Goolsbee, have argued that wage gains say little

about future price increases, but largely reflect past price hikes.

Atlanta Fed economists have cast it differently still, saying that after

COVID-19 pandemic years in which businesses saw outsized profits, there

is room for wages to grow through a decline in business margins rather

than a rise in prices.

In a joint appearance with Bernanke at a U.S. central bank research

conference last Friday, Fed Chair Jerome Powell seemed to have settled

in a place similar to the former Fed leader, saying that much of the

work left to be done in lowering inflation will have to come from a job

market still sustaining a 3.4% unemployment rate, abnormally high

numbers of vacancies, and wage gains outpacing the rate of price

increases.

"I don't think labor market slack was a particularly important feature

of inflation when it first spiked in spring of 2021," Powell said. "By

contrast, I do think that labor market slack is likely to be an

increasingly important factor in inflation going forward," reiterating

his observation that price increases are proving most stubborn in

service industries where "labor costs are a high proportion of total

costs."

[to top of second column] |

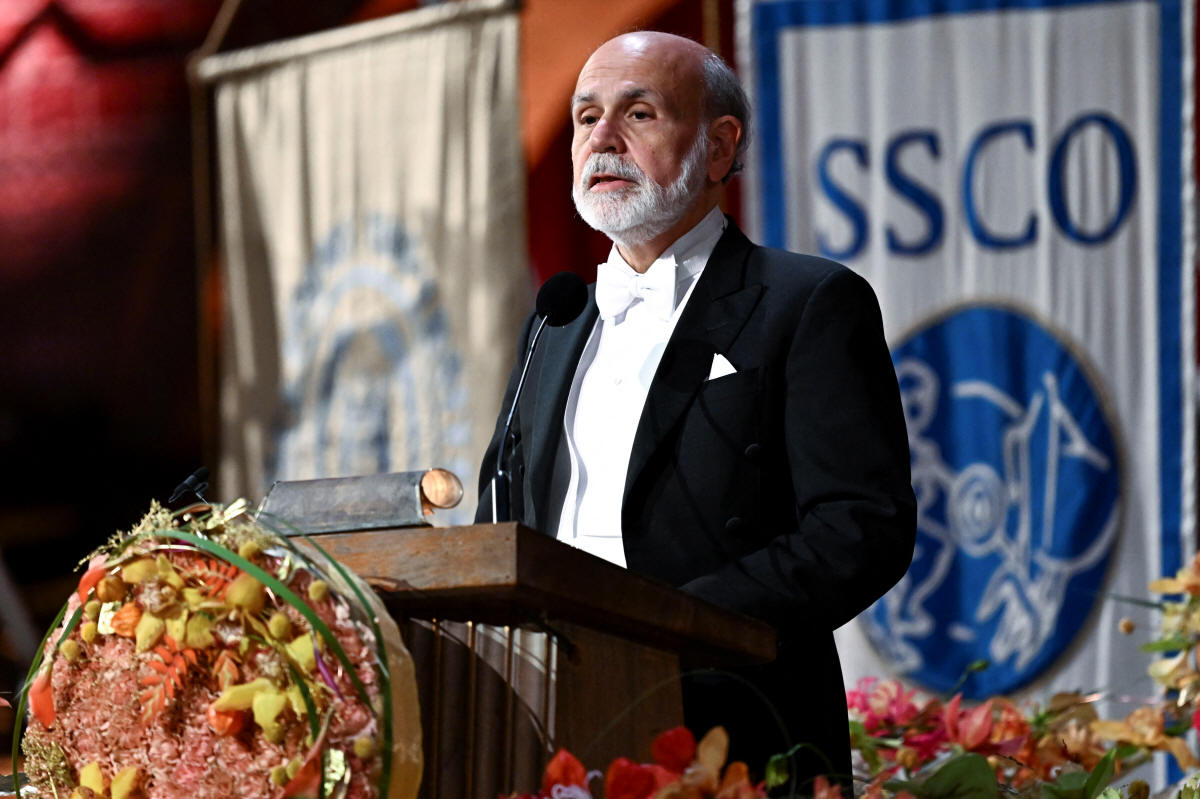

Nobel laureate in Economic Sciences Ben

S. Bernanke speaks during the Nobel Prize Banquet at the Town Hall

in Stockholm, Sweden December 10, 2022. TT News Agency/Jonas

Ekstromer via REUTERS

A Fed intent on producing weaker hiring and slower wage growth

would, at least in the past, imply rising joblessness. Indeed,

policymakers expect the unemployment rate to increase as their fight

against inflation continues.

How fast and by how much remains a contested point: Some outside

economists have estimated unemployment rates as high as 6% or 7%

will be necessary, while Fed policymakers remain hopeful of a more

modest dislocation.

Bernanke and Blanchard did not take an explicit stand on that issue,

but said it may still be possible for the labor market to ease

largely through a drop in the number of job openings rather than a

rise in joblessness.

INFLATION EXPECTATIONS

Their study, however, points to some of the risks Fed officials may

face as they decide whether to be patient in allowing time for

inflation to slow, or use further rate increases to force a faster

adjustment in an effort to ensure high inflation does not become

embedded.

Bernanke and Blanchard estimate that inflation could return to the

Fed's 2% annual target if over the next two years their preferred

measure of labor market slack - the number of job openings for each

unemployed job seeker - falls below 1 to around 0.8, meaning more

unemployed workers are competing for jobs than there are open

positions.

If over that time the ratio falls only to the pre-pandemic rate of

around 1.2, by contrast, inflation as measured by the Consumer Price

Index would fall to around 2.7% - still high, but "within striking

distance" of the Fed's 2% target, the authors said, given the

differences between the CPI and the Personal Consumption

Expenditures Price Index the Fed prefers.

But "allowing (the ratio) to remain near current levels does not

bring inflation down in our projections. Indeed, because an extended

period of inflation raises long-term inflation expectations, it

leads to slowly increasing inflation," they wrote.

The current ratio is 1.6, down from a peak of around 2 last year.

"The portion of inflation which traces its origin to overheating of

labor markets can only be reversed by policy actions that bring

labor demand and supply into better balance," Bernanke and Blanchard

concluded. "Labor market balance should ultimately be the primary

concern for central banks attempting to maintain price stability."

(Reporting by Howard Schneider; Editing by Dan Burns and Paul Simao)

[© 2023 Thomson Reuters. All rights

reserved.]

This material may not be published,

broadcast, rewritten or redistributed.

Thompson Reuters is solely responsible for this content.

|