Productivity adds the anesthetic to Powell's pain-free disinflation

Send a link to a friend

Send a link to a friend

[November 03, 2023] By

Howard Schneider [November 03, 2023] By

Howard Schneider

WASHINGTON (Reuters) - A recent surge in U.S. productivity has

underscored Federal Reserve Chair Jerome Powell's emerging narrative for

how inflation may continue to decline even amidst sustained job and

economic growth.

The best-of-both-worlds outcome would rely on the U.S. finding a new

balance between the demand for and the supply of goods and services less

by "destroying" demand - the way Fed interest rate increases typically

play out - and more through improvements in the economy's capacity.

In what has been a somewhat unheralded surprise, that is what has been

unfolding through both improvements in the number of people willing to

work, including new immigrants, and also through improvements in how

much each worker produces, a dynamic that lowers effective labor costs

even if wages are higher.

New data released Wednesday showed productivity grew an outsized 4.7% in

the third quarter, the largest increase in three years and the second

large gain this year. That caused unit labor costs to fall at a 0.8%

annualized rate.

The net result is higher potential output with less inflationary risk,

something Powell pointed to on Wednesday in his most extensive comments

to date on the possibility that for the moment at least the economy may

have an enhanced ability to grow, add jobs, and raise wages without

adding to inflation.

The October employment report due on Friday at 8:30 EDT (1230 GMT) will

provide updated estimates of the size of the labor force, a critical

piece of the puzzle. After stalling through much of 2022, the workforce

grew by 3 million workers, or about 2%, in the nine months through

September.

The dynamic is one reason why the Fed kept its policy interest rate on

hold at 5.25%-5.50% at its meeting this week despite recent data showing

the economy grew at a 4.9% annualized rate in the third quarter - far

beyond the 1.8% rate Fed officials see as the underlying long-term,

noninflationary trend.

Throughout the pandemic era growth has largely exceeded that rate even

as inflation has continued to fall, and Powell at his post-meeting press

conference on Wednesday tried to square the circle.

"People think trend growth over a long period of time is a little less

than 2%," Powell said. But "potential growth is elevated for a year or

two right now over its trend level...you're seeing actually elevated

potential growth, catch up growth, that can happen" because of

improvements in things like labor supply that, all things equal, allow

the economy to grow faster without the same price pressures. Along with

more people working, productivity adds a boost as well.

CAN IT LAST?

Higher potential growth provides more leeway for the economy to grow

without the Fed worrying about the impact on prices. In other words, it

offers a wider runway for the "soft landing" Fed officials have hoped to

engineer with inflation falling but the economy largely left on track.

[to top of second column] |

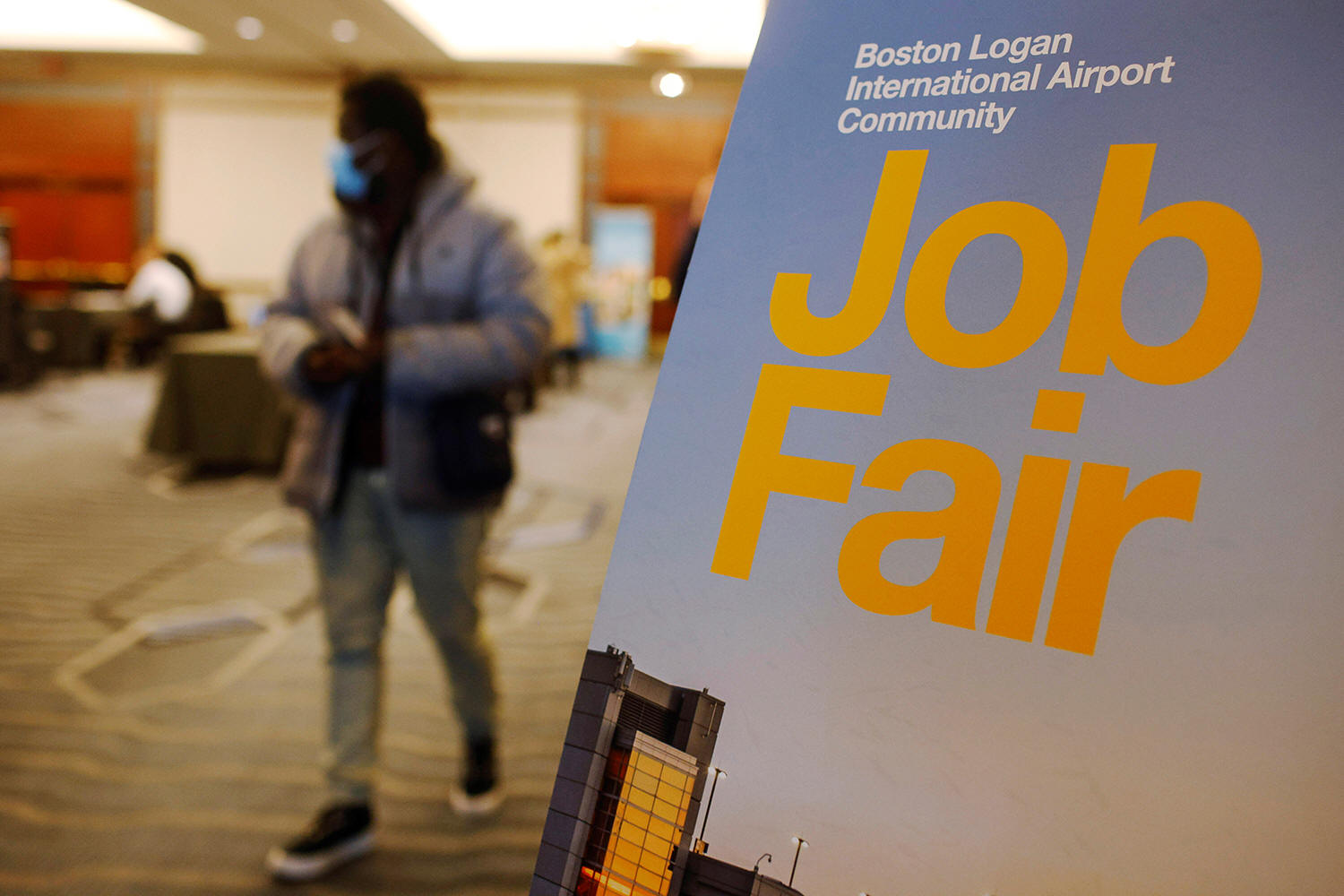

A job seeker leaves the job fair for airport related employment at

Logan International Airport in Boston, Massachusetts, U.S., December

7, 2021. REUTERS/Brian Snyder

Rising productivity "signals receding inflationary pressure even as

the economy continues to display notable resilience," said EY Senior

Economist Lydia Boussour. "If companies can generate strong

productivity growth, they will not be so inclined to pass elevated

input costs onto consumers."

The Fed's situation mimics in some ways the mid-1990s, when Alan

Greenspan - the central bank's chief at the time - resisted pressure

to raise interest rates, arguing that rising productivity would let

the economy grow with less inflation, an insight credited with

keeping that decade's strong economic performance on track.

The spread of Web-based technologies was still in its relative

infancy then, and the years since have produced not only more

tempered productivity numbers, but a generally dismal assessment

that trend growth in output per worker hour was only around 1.5%.

That, coupled with sluggish population growth, is the reason Fed

officials in recent years have steadily downgraded their view of the

long-term trend growth in overall economic output, with the median

fixed at around 1.8% since 2016.

Powell and his colleagues must now decide just how sustainable the

recent improvements are.

The upside, as Powell described it, is the possibility of a virtuous

cycle developing in which jobs remain plentiful, wages grow, and the

economy continues to expand - all with a steady "disinflation" as

the pace of price pressures fall back to 2%.

"The dynamic has been really strong job creation, with wages that

are higher than inflation...and that raises real disposable income,

that raises spending, which continues to drive more hiring," Powell

said. "It has been good. And the thing is, we've been achieving

progress on inflation in the middle of this.

"The question is, how long can that continue?"

If and when it stops, the Fed may face the tougher choice of just

how much the economy - the demand side at least - needs to slow to

keep inflation in line.

"Growth is going to be slower this quarter...Higher rates are

dampening activity here and there," wrote TSLombard Chief U.S.

Economist Steven Blitz. But "if real growth continues apace,

disinflation runs its course and enough inflation eventually returns

to pull the Fed back into a tightening cycle."

(Reporting by Howard Schneider; Editing by Dan Burns and Andrea

Ricci)

[© 2023 Thomson Reuters. All rights

reserved.]

This material may not be published,

broadcast, rewritten or redistributed.

Thompson Reuters is solely responsible for this content. |