Morning Bid: Rate-cut hopes meet Mid-East risks

Send a link to a friend

Send a link to a friend

[August 26, 2024] A

look at the day ahead in U.S. and global markets by Dhara Ranasinghe. [August 26, 2024] A

look at the day ahead in U.S. and global markets by Dhara Ranasinghe.

Not for the first time, financial markets are reminded why it's never a

good idea to get too far ahead.

So, while Federal Reserve chief Jerome Powell's much-awaited Jackson

Hole speech on Friday fueled the rate-cut optimism that has aided

stocks' recovery from the early-August rout, the latest Middle East news

highlights the need for caution.

Hezbollah launched hundreds of rockets and drones at Israel early on

Sunday, as Israel's military said it struck Lebanon with around 100 jets

to thwart a larger attack, in one of the biggest clashes in more than 10

months of border warfare.

Any major spillover in the fighting, which began in parallel with the

war in Gaza almost a year ago, risks morphing into a regional

conflagration drawing in Hezbollah's backer Iran and Israel's main ally

the United States.

Iran's foreign minister was reported saying the country does not seek to

increase Middle East tensions. Still, a rise of more than 1% in oil

prices suggests some unease among investors that regional oil supplies

could face disruption.

A full read out of the mood music is difficult with London markets

closed for a public holiday.

Still, European shares are flat, as are U.S. stock futures, while

Japan's blue-chip Nikkei closed the Asia session down almost 0.7%.

JACKSON HOLE

The more hesitant tone in world markets follows a fresh surge in

optimism that a U.S. rate cutting cycle is likely to begin in September.

In highly anticipated comments before the Jackson Hole Economic

Symposium, Fed boss Powell said "the time has come" to lower the Fed

funds target rate, and "the upside risks of inflation have diminished."

[to top of second column] |

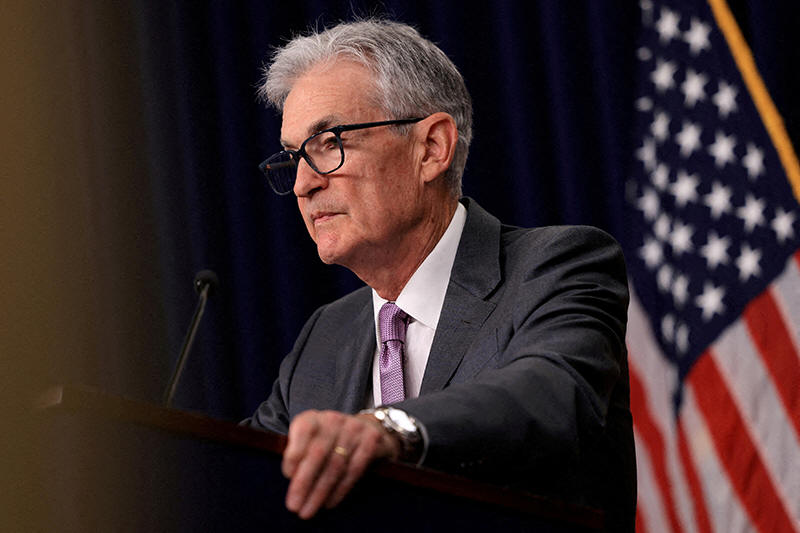

U.S. Federal Reserve Chair Jerome Powell speaks during a press

conference following a two-day meeting of the Federal Open Market

Committee on interest rate policy in Washington, U.S., July 31,

2024. REUTERS/Kevin Mohatt/File Photo

For sure, the data-dependent Fed will have a raft of economic

indicators to consider ahead of its September meeting, including

this week's revised second-quarter GDP and the broad-ranging

Personal Consumption Expenditures (PCE) report, which includes the

Fed's preferred inflation yardstick, the PCE price index.

But these would have to deliver major surprises to shake the

market's view that a rate decrease -- of at least 25 basis points --

is coming.

Also speaking at Jackson Hole, European Central Bank chief economist

Philip Lane struck a more cautious note at the weekend, saying the

central bank was making "good progress" in cutting euro zone

inflation back to its 2% target but success is not yet assured.

All this has left the dollar languishing at three-week lows versus

the yen. The euro and British pound were a tad lower on the day but

holding near multi-month peaks hit against the greenback on Friday.

Key developments that should provide more direction to U.S. markets

later on Monday:

* German August Ifo index falls in August.

* U.S. July durable goods due out.

(Reporting by Dhara Ranasinghe; Editing by Toby Chopra)

[© 2024 Thomson Reuters. All rights

reserved.]

This material may not be published,

broadcast, rewritten or redistributed.

Thompson Reuters is solely responsible for this content.

|