How the wildfires in the Los Angeles area could affect California's home

insurance market

Send a link to a friend

Send a link to a friend

[January 10, 2025] By

TRÂN NGUYỄN [January 10, 2025] By

TRÂN NGUYỄN

SACRAMENTO, Calif. (AP) — The wildfires that destroyed homes in multiple

sections of the Los Angeles area will test California’s efforts to

stabilize the state’s insurance marketplace after many insurers stopped

issuing residential policies due to the high fire risk.

The wind-driven blazes that started Tuesday roared through neighborhoods

from the Pacific Coast inland to Pasadena and the Hollywood Hills. The

vast property damage in a disaster-prone state with high real estate

prices and an uncertain insurance landscape could make coverage more

expensive and even harder to find.

One area likely to feel the impact — and encounter challenges rebuilding

— is Pacific Palisades, an affluent community sandwiched between the

Pacific Ocean and the Santa Monica Mountains. This week's wildfire there

has been named as the most destructive in the modern history of the city

of Los Angeles. Flames destroyed businesses, a library, cultural

landmarks as well as houses.

State authorities previously listed the Palisades as one of the five

Southern California areas with the highest concentration of potential

wildfire risks. The community also is among the areas most impacted by

an unavailability of insurance coverage.

When State Farm decided to discontinue coverage for 72,000 houses and

apartments in California last year, it dropped nearly 70% of its market

share in Pacific Palisades, according to the San Francisco Chronicle.

Here's what to know about California's residential insurance crisis and

how the ongoing wildfires may further disrupt the policy market:

Why does California have a home insurance crisis?

California has seen other major insurers pull back on property coverage

in the nation's most populous state as climate change makes wildfires,

floods and windstorms more common and damaging.

Of the top 20 most destructive wildfires in state history, at least 15

occurred since 2015. The data did not include the Los Angeles area fires

this week.

In 2023, seven of the 12 largest insurance companies by market share in

California either paused or restricted issuing new policies in the

state.

That has made it extremely difficult for homeowners in high-risk areas

to obtain or afford insurance.

What happens to residents who can't get regular home insurance?

California homeowners in wildfire-prone areas either go without

insurance or join the Fair Access to Insurance Requirements (FAIR) Plan,

which the state created as a last resort for homeowners who couldn't

find insurance.

Many people purchase the FAIR Plan to satisfy their mortgage

requirements, but the policies only cover basic property damage and

carry a $3 million limit. Given the value of the real estate involved

and the limited coverage, FAIR Plan policyholders who lost homes in this

week's fires may struggle to be made whole.

The policies can be very bare bones, with some options only covering the

actual cash value of what was lost rather than the true replacement

costs, said Amy Bach, executive director of the consumer advocacy group

United Policyholders.

The plan was designed to be a temporary solution, but more Californians

are relying on it than ever. The number of FAIR residential policies

issued in the state more than doubled between 2020 and 2024, reaching

nearly 452,000 policies.

Could claims from the LA fires push the FAIR Plan into insolvency?

Policies sold to FAIR customers primarily fund the plan, but insurers

would have to pay into the fund if it becomes insolvent or to keep it

from insolvency. Under a new state rule, insurers could ask the state to

approve rate increases to recoup the money spent on bailing out the FAIR

Plan.

FAIR Plan spokesperson Hilary McLean said it could take years to tally

total losses from the Los Angeles area fires. While it's too soon for

reliable loss estimates, the FAIR Plan anticipates being able to pay out

claims from the wildfires, McLean said.

[to top of second column] |

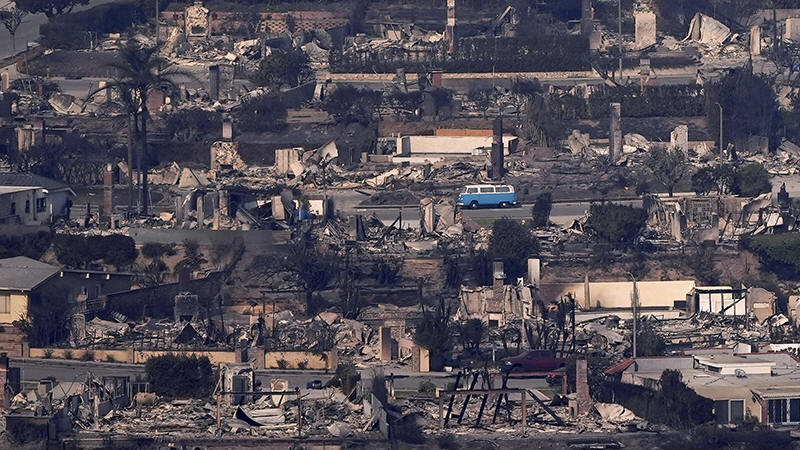

A VW van sits among burned out homes, Thursday, Jan. 9, 2025, in

Malibu, Calif. (AP Photo/Mark J. Terrill)

“We are aware of misinformation

being posted online regarding the FAIR Plan’s ability to pay

claims," she said in a statement. "The FAIR Plan has payment

mechanisms in place, including reinsurance, to ensure all covered

claims are paid.”

The plan has roughly $700 million in cash on hand and about $2.5

billion in reinsurance, according to testimony given to California

lawmakers last year.

The mean home value in Pacific Palisades and its surrounding areas

hovers around $3.3 million, according to real estate company Redfin.

Owners of the most valuable properties probably are not relying on

the FAIR Plan because of the coverage limit, said Jamie Court,

president of nonprofit organization Consumer Watchdog.

The claims from the fires will be significant, Court said, “but this

is not enough to put the industry out of business or the FAIR Plan

out of business.”

On Thursday state lawmakers introduced a bill that would give the

FAIR Plan the ability to seek “catastrophe bonds” if it faces

liquidity challenges.

How has California responded to the insurance crisis?

In a new tactic, state officials undertook a yearlong overhaul to

give insurers more latitude to raise premiums in exchange for more

issuing policies in high-risk areas.

A new regulation that took effect this month allows insurers to

consider climate change when setting their prices. California

previously did not let insurance companies factor in current or

future risks when deciding how much to charge. Many companies cited

the restriction as their reason for retreating from the state's

insurance market.

The state is also in the final stage of approving a rule that would

let insurance companies pass on the costs of reinsurance to

California consumers. Insurance companies typically buy reinsurance

— or insurance for themselves — in case they face huge payouts from

natural disasters or catastrophic losses. California is the only

state that doesn’t already allow the cost of reinsurance to be borne

by policyholders.

The new rules have prompted Farmers, the second-largest insurer in

the state, to resume writing new policies for homeowners last month.

Consumer Watchdog's Court says the rules also could make it easier

for insurers to raise rates with little oversight.

How will the fires impact California's insurance market?

It's “premature” to assess whether the wind-whipped fires and their

destruction will put a damper on California's attempt to preserve

home insurance options for residents, said Denneile Ritter, a vice

president with the American Property Casualty Insurance Association,

the largest national trade association for home, auto and business

insurers.

But higher homeowner premiums could be coming soon, RAND economist

Lloyd Dixon said. If insurers' models signal a potential increase of

risk, “then you’d expect to see the requests for premium increases

by the insurers,” he said.

California Insurance Commissioner Ricardo Lara said Wednesday that

the newly enacted rules allowing climate change consideration in

premiums will help insurers accurately assess risks and set fair

rates. The state is also issuing a one-year moratorium prohibiting

insurance companies from dropping coverage in areas affected by

fires.

“Insurance companies are pledging their commitment to California,

and we will hold them accountable for the promises they have made,”

Lara said in a statement.

___

Associated Press writer Sally Ho in Seattle contributed.

All contents © copyright 2024 Associated Press. All rights reserved |